Uninsured Motorist Coverage Explained: Protect Your Finances

- Guyorguy Laguerre

- 4 days ago

- 11 min read

TL;DR:

Uninsured motorist coverage pays for your damages when the at-fault driver lacks insurance or flees.

Many drivers are underinsured, risking large out-of-pocket expenses after serious accidents.

Choosing appropriate UM limits and regularly reviewing your policy are essential for adequate protection.

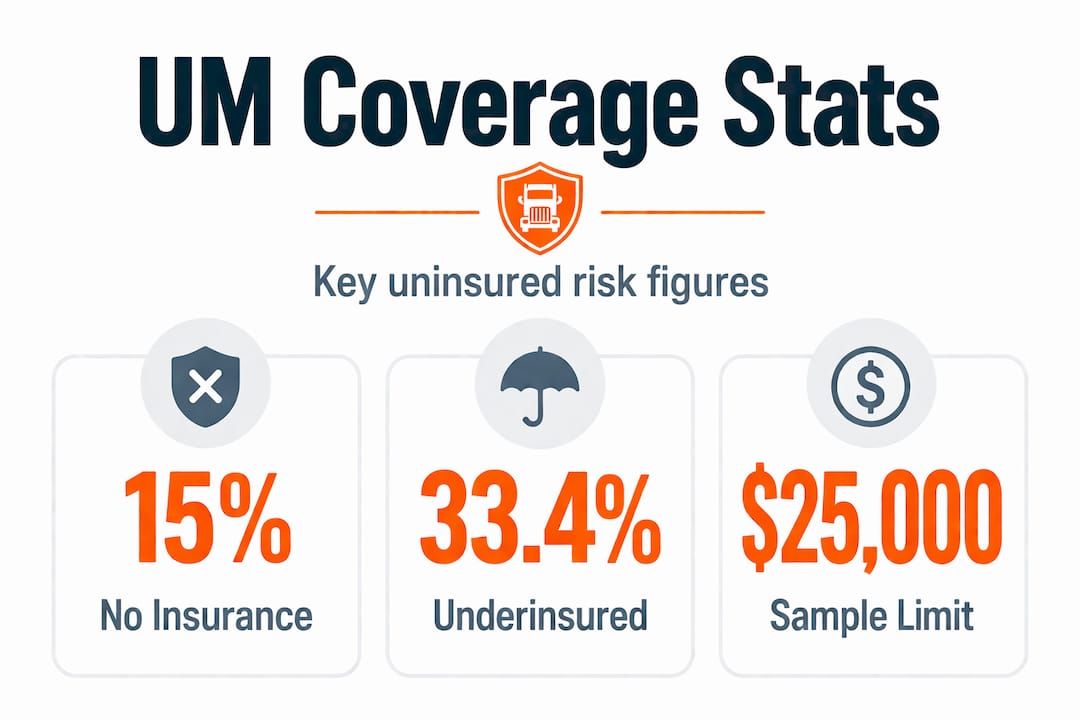

Most drivers hit the road assuming everyone around them carries valid auto insurance. That assumption is expensive when it’s wrong. 15.4% of drivers were uninsured in 2023, which means roughly one in six cars sharing the road with you has no coverage. If one of those drivers causes an accident, your standard liability policy won’t help you recover a single dollar. Uninsured motorist coverage, commonly called UM coverage, is the policy layer that fills that gap. This article breaks down exactly what it is, how it works, and how to make smart decisions about protecting your finances.

Table of Contents

Key Takeaways

Point | Details |

High risk of uninsured drivers | Over 15% of U.S. drivers lack insurance, increasing accident risks. |

Personal financial protection | UM coverage pays your bills if the other driver cannot. |

Know your coverage limits | Low limits can leave you paying out of pocket after severe accidents. |

Special concerns for businesses | Fleets and business vehicles face unique UM coverage needs. |

Get expert advice | Insurance professionals can help you select the right UM protection. |

What is uninsured motorist coverage?

Uninsured motorist coverage is a type of auto insurance protection that pays for your losses when a driver who caused an accident carries no insurance at all. It flips the normal claims process on its head. Instead of filing against the at-fault driver’s policy, you file against your own. Your insurer steps in to cover what the other driver legally owes you but cannot pay.

This matters because the traditional system assumes the person who caused the crash has insurance to cover your damages. When they don’t, you’re left holding the bill unless you have UM coverage in place.

What UM coverage typically pays for:

Medical bills and hospital costs for you and your passengers

Lost wages if injuries prevent you from working

Pain and suffering in many states

Funeral expenses in fatal accident cases

Rehabilitation and long-term care costs

UM claims are first-party claims that you pursue with your own insurer up to your UM policy limits. That’s a critical distinction. You’re not suing the uninsured driver directly, at least not as your first move. You’re working with your own insurance company to get compensated.

There are two closely related terms you’ll see on most policies. Uninsured motorist coverage (UM) applies when the at-fault driver has zero insurance. Underinsured motorist coverage (UIM) applies when the at-fault driver has some insurance, but not enough to cover your actual losses. Many policies bundle both together under a single UM/UIM designation, though some states treat them separately.

Understanding the difference between a first-party claim and a third-party claim is important here. A third-party claim goes to someone else’s insurer. A first-party claim goes to your own. UM coverage makes your insurer responsible for compensating you, which generally speeds up the process and removes the need to chase an uninsured driver through civil court.

Why uninsured motorist coverage matters: The real risks

Defining UM coverage is just the start. Understanding its importance means looking at the current risks on the road.

The numbers are genuinely alarming. 33.4% of drivers were uninsured or underinsured in 2023 when you combine both categories. That means one in three drivers you encounter may not have enough coverage to pay for a serious accident they cause. These aren’t just statistics. They represent real situations where accident victims end up with unpaid medical bills, lost income, and vehicles they can’t afford to repair.

Consider a realistic scenario. You’re stopped at a red light when another driver rear-ends your car at 40 miles per hour. You suffer a herniated disc requiring surgery. Your car is totaled. You miss three months of work. Total losses easily reach $80,000 or more. If the at-fault driver has no insurance, your only recourse without UM coverage is to sue them personally. Most uninsured drivers don’t have significant assets to collect. You could win a judgment in court and still collect nothing.

Hit-and-run accidents add another layer of risk. In many states, UM coverage also applies when the at-fault driver flees the scene and can’t be identified. That means even ghost accidents, where you never get a license plate number, can still be covered under your UM policy.

How different types of drivers and businesses are affected:

Situation | Risk without UM | Protection with UM |

Individual driver | Pays medical bills out of pocket | Insurer covers medical costs up to limits |

Family with multiple vehicles | Multiple people exposed | All listed drivers typically covered |

Small business with one vehicle | Business absorbs all losses | Policy covers employee injuries and losses |

Commercial fleet operator | High exposure across many drivers | Fleet UM policy covers multiple vehicles |

Rideshare or delivery driver | Gap between personal and commercial | Specialized UM may be needed |

“One in three drivers on the road may not have enough insurance to cover a serious accident. That’s not a rare edge case. That’s a daily reality every time you drive.”

State laws vary significantly. Some states require UM coverage as a mandatory part of every auto policy. Others make it optional but require insurers to offer it. A handful of states have minimal requirements that leave drivers surprisingly exposed. Knowing your state’s rules is important, but relying on the legal minimum is rarely the smartest financial move.

Commercial fleet operators face a compounded version of this risk. Every driver in a fleet is exposed to uninsured motorists every single day. If you manage vehicles for a business, understanding insurance for trucking companies is essential because the financial exposure from a single serious accident can threaten the entire operation.

Pro Tip: Don’t just check whether your state requires UM coverage. Check what your state’s minimum limits actually are. In many states, the required minimums are far too low to cover a serious accident in 2026.

How uninsured motorist coverage protects you

Understanding the risks is key. Now let’s see exactly how UM coverage steps in to protect you financially.

UM coverage has two main components that most policies separate clearly. Uninsured motorist bodily injury (UMBI) covers medical expenses, lost wages, and pain and suffering for you and your passengers. Uninsured motorist property damage (UMPD) covers damage to your vehicle. Not every state requires both, and not every policy automatically includes UMPD, so reading your declarations page carefully is essential.

Step-by-step: How to file a UM claim

Report the accident to local law enforcement immediately. A police report creates an official record that the accident happened and that the other driver was uninsured or fled the scene.

Document everything at the scene. Photographs of vehicle damage, your injuries, the other driver’s license plate if available, and witness contact information all strengthen your claim.

Notify your insurer promptly. Most policies require you to report accidents within a specific time window. Delaying notification can jeopardize your claim.

File the UM claim directly with your own insurance company. Provide all documentation including the police report, medical records, and any evidence of lost income.

Work with your insurer’s adjuster. They will evaluate your claim, review your medical bills, and determine what falls within your UM policy limits.

Negotiate if necessary. If your insurer’s initial offer doesn’t cover your actual losses, you have the right to negotiate or seek legal counsel.

Receive payment up to your UM coverage limits once the claim is settled.

You file a claim with your own insurance company, which reimburses you up to the UM/UIM limits you selected when you purchased the policy. This is why choosing the right limits upfront matters so much.

Typical UM coverage limits and what they mean:

Coverage limit | What it pays (per person/per accident) | Common gap scenario |

$25,000 / $50,000 | Low protection for minor injuries | Insufficient for surgery or long recovery |

$50,000 / $100,000 | Moderate protection | May cover most injuries but not severe cases |

$100,000 / $300,000 | Strong individual protection | Covers most serious accident scenarios |

$250,000 / $500,000 | High protection for serious losses | Best for families and high-income earners |

Coverage limits are expressed as per-person and per-accident maximums. If your limit is $50,000 per person and your medical bills reach $90,000, you pay the $40,000 difference out of pocket. That’s why selecting limits that reflect your actual financial exposure is so important.

For businesses operating vehicles, the stakes are even higher. A single accident involving an employee can trigger workers’ compensation claims, liability exposure, and vehicle repair costs simultaneously. Understanding commercial auto insurance basics helps fleet managers see how UM fits into a broader risk management strategy rather than treating it as an afterthought.

Exclusions are real and worth knowing. Most UM policies won’t cover damage to personal property inside the vehicle, punitive damages, or accidents that happen while the vehicle is being used for unauthorized commercial purposes. Reading the fine print before you need to file a claim saves enormous frustration later.

Key decisions: Choosing and using UM coverage wisely

Knowing how UM works, you’re ready to make informed decisions. Here’s how to choose and use the right coverage.

The single biggest mistake most drivers make is treating UM coverage as a checkbox rather than a financial decision. They select the state minimum, pay the lowest premium, and assume they’re covered. They’re not wrong technically. But low UM limits can leave you facing out-of-pocket losses after serious crashes that the minimum simply cannot absorb.

Common pitfalls to avoid:

Choosing minimum limits without calculating your actual risk. If you earn $80,000 per year and suffer injuries that keep you out of work for six months, a $25,000 UM limit covers less than two months of income replacement.

Forgetting to update your policy after life changes. Getting married, having children, or buying a new home all increase your financial exposure. Your UM limits should reflect your current situation, not the one you had three years ago.

Assuming your health insurance will cover everything. Health insurance covers medical bills but not lost wages, pain and suffering, or vehicle repairs. UM and health insurance serve different purposes.

Not understanding your state’s stacking rules. Some states allow you to “stack” UM coverage across multiple vehicles on the same policy, effectively multiplying your coverage. Others don’t. Knowing your state’s rules could significantly change how much protection you actually have.

Ignoring hit-and-run scenarios. Many drivers don’t realize UM coverage often applies to hit-and-run accidents where the at-fault driver is never identified. This is one of the most valuable and overlooked aspects of UM coverage.

When UM is legally required, your insurer must include it in your policy unless you sign a written waiver declining it. That waiver is a serious document. Signing it to save a few dollars per month can cost you tens of thousands in a real accident.

For individuals, the right UM limit depends on your income, assets, family size, and health insurance coverage. A single person with strong employer health coverage and modest income has different needs than a family of five where one parent is self-employed.

For fleets and commercial operators, the calculation is more complex. Each vehicle represents a separate exposure point, and the drivers operating those vehicles may have very different risk profiles. Reviewing fleet insurance options with a licensed professional helps businesses build a UM strategy that covers all their vehicles without leaving dangerous gaps.

Pro Tip: Ask your insurance professional about umbrella policies. A personal umbrella policy can extend your UM coverage beyond your auto policy limits in some states, giving you an extra layer of protection for a relatively modest additional premium.

Reviewing your UM coverage annually is a smart habit. Insurance markets change, your personal situation evolves, and state laws occasionally update. A quick annual review with a licensed professional ensures your coverage keeps pace with your actual life.

Don’t assume: The real takeaway on uninsured motorist coverage

Here’s a perspective that most articles on this topic won’t give you directly. The people who get hurt the most by inadequate UM coverage are not reckless drivers or people who ignore insurance entirely. They’re careful, responsible people who bought what they thought was solid coverage, never looked closely at the limits, and discovered the gap only when they needed the money most.

Claims adjusters and insurance professionals see this pattern constantly. A policyholder carries $25,000 in UM bodily injury coverage because that’s what the state required when they first bought the policy years ago. They never updated it. Then a serious accident happens, bills climb past $100,000, and the shock of learning their coverage maxes out at $25,000 is genuinely devastating.

The uncomfortable truth is that mandatory insurance requirements are designed to create a baseline, not to protect you adequately. States set minimums based on political and economic compromises, not based on what a real accident actually costs in 2026. Medical inflation has pushed surgical costs, hospital stays, and rehabilitation expenses far beyond what older minimum limits anticipated.

Fleet owners face a version of this problem that’s even more acute. Many small trucking operations and delivery businesses focus heavily on liability coverage because that’s what protects them from lawsuits. UM coverage, which protects their drivers, sometimes gets treated as secondary. But drivers are the most valuable asset in any fleet operation. An injured driver who can’t work creates costs that go far beyond the medical bills. There’s lost productivity, potential workers’ compensation claims, and the human cost of someone whose livelihood is disrupted.

The advice that insurance professionals wish more people would internalize is simple. Think about UM coverage not as a regulatory requirement but as income replacement insurance for the scenario where someone else’s irresponsibility costs you your ability to earn. When you frame it that way, the decision to carry higher limits becomes much easier to justify.

Reviewing insurance tips for businesses alongside your personal auto coverage review gives you a fuller picture of how UM fits into a complete risk management approach, whether you’re protecting your family or your business.

Get expert help with uninsured motorist coverage

Understanding UM coverage is a meaningful first step, but translating that knowledge into the right policy for your specific situation requires professional guidance. Every driver’s risk profile is different, every state’s rules are different, and the right UM limits for a single driver in a low-risk area look very different from what a commercial fleet operator in a high-traffic metro needs.

Insuaria is built to make that next step easier. Through simple intake forms and educational resources, Insuaria helps you organize the details that licensed insurance professionals need to review your coverage situation. Whether you’re an individual wondering if your current UM limits are adequate, a family reassessing coverage after a life change, or a business owner trying to protect your fleet and your drivers, submitting your information through insurance inquiry help connects you with licensed agency partners who can review your needs and follow up with real guidance. Take a few minutes to get a UM coverage review and find out whether your current policy is actually protecting you or just checking a box.

Frequently asked questions

Is uninsured motorist coverage required in all states?

No, requirements vary by state. Many states require UM coverage as part of every auto policy, but some make it optional or allow drivers to waive it in writing. Always check your specific state’s current requirements.

What does uninsured motorist coverage typically cover?

UM coverage typically covers medical bills, lost wages, and sometimes pain and suffering when you’re injured by a driver who has no insurance. Property damage coverage for your vehicle may also be included depending on your policy and state.

Can I upgrade my uninsured motorist coverage limits at any time?

You can usually request changes to your UM limits when you renew your policy or by contacting your insurance company directly. Some insurers allow mid-term changes, though timing and availability depend on your specific policy terms.

How do I file a claim with uninsured motorist coverage?

UM claims are first-party claims you file directly with your own insurer after an accident involving an uninsured driver. Report the accident promptly, gather documentation, and work with your insurer’s claims team to process the claim up to your policy limits.

Does uninsured motorist coverage apply to hit-and-run accidents?

In many states, yes. UM coverage often applies when the at-fault driver flees the scene and cannot be identified, though specific rules and documentation requirements vary by state and policy. A police report is typically required to support a hit-and-run UM claim.

Recommended

Comments