Insurance for Refrigerated Trucking: 2026 Fleet Guide

- Guyorguy Laguerre

- May 19

- 10 min read

TL;DR:

Standard cargo insurance often excludes refrigeration failure-related spoilage, requiring specialized endorsements to cover losses. Proper operational practices, documentation, and advanced monitoring significantly impact insurance costs and claim success for refrigerated trucking. Working with specialized insurance providers and preparing complete claim records can safeguard loads and optimize coverage.

If you haul perishable goods and rely on a standard commercial truck policy, you may be carrying a coverage gap that could cost you an entire load. Insurance for refrigerated trucking is a specialized category, and what protects a dry van carrier simply does not protect a reefer operation. Temperature excursions, mechanical breakdowns, spoiled pharmaceuticals, and cargo that arrives warm instead of frozen each create liabilities that standard truck insurance was never designed to handle. This guide breaks down exactly which coverages you need, what they cost, and how to manage your operation to protect every load you haul.

Table of Contents

Key takeaways

Point | Details |

Standard coverage falls short | Standard motor truck cargo insurance excludes spoilage from refrigeration failure; a reefer breakdown endorsement must be added explicitly. |

Costs vary widely by cargo type | Pharmaceutical refrigerated transport insurance can run $3,000 to $6,000 per unit annually, far above standard frozen food rates. |

Documentation protects your claims | Insurers require temperature logs, maintenance records, and mitigation proof before paying a temperature excursion claim. |

Regional factors drive premiums | Florida refrigerated truck insurance averages $5,000 to $14,000 per truck annually due to extreme heat and elevated spoilage risk. |

Compliance unlocks better rates | FSMA, FDA, and driver training compliance can qualify your fleet for preferred pricing from specialized carriers. |

Insurance for refrigerated trucking: core coverage types

Most fleet managers assume their motor truck cargo policy covers whatever is in the trailer. For dry freight, that assumption is mostly correct. For refrigerated freight, it is the wrong assumption to make, and it can be a very expensive one.

Standard cargo insurance excludes spoilage caused by refrigeration equipment failure. That means if your reefer unit fails on a summer run and you lose a full trailer of frozen meat or produce, a basic cargo policy will likely deny the claim. The spoilage happened because of equipment failure, not because of collision, theft, or the other named perils a standard policy typically covers.

Reefer breakdown coverage

A reefer breakdown endorsement is the add-on that fills this gap. It extends your cargo policy to include losses caused by the sudden and accidental failure of the refrigeration unit itself. Think compressor seizure, electrical failure, or a refrigerant leak that sends temperatures into an unsafe range while your driver is on a long haul.

Reefer breakdown endorsements cost between $500 and $2,000 per year added to your cargo policy, and while no federal regulation mandates this coverage, most shippers and freight brokers now require it as a contract condition. Refusing to carry it does not save money. It costs you freight contracts.

Motor truck cargo with spoilage endorsements

Here is what the coverage hierarchy looks like for a properly insured reefer operation:

Motor truck cargo insurance provides the base layer, covering cargo loss from accidents, theft, and fire.

Reefer breakdown endorsement adds coverage for cargo loss specifically caused by refrigeration equipment failure.

Physical damage coverage protects the truck and trailer from collision, rollover, and weather events.

Commercial auto liability covers bodily injury and property damage you cause to third parties.

Loading and unloading endorsements address the liability window when cargo is being transferred, a commonly overlooked exposure point for perishable goods.

Common exclusions that catch operators off guard

Even with the right endorsements in place, certain losses will not be covered. Coverage exclusions for operator error, improper maintenance, and delayed reporting are standard across the industry. If your driver ignores a temperature alarm and the load spoils over six hours before anyone acts, the insurer will likely treat that as operator error and deny the claim.

ATP certification for refrigeration units and documented routine maintenance programs are not just operational best practices. They are coverage requirements for many carriers. If you cannot prove the unit was certified and maintained, the insurer has grounds to walk away from the claim.

Pro Tip: Request a written confirmation from your insurer listing every exclusion that applies to your reefer endorsement before binding coverage. Surprises on exclusions show up at claim time, not at renewal.

What refrigerated trucking insurance actually costs

Cost is where most fleet managers get either surprised or confused. Insurance for refrigerated trucking does not follow the same pricing logic as dry freight coverage, and the range is genuinely wide depending on what you haul, where you operate, and how well your fleet is managed.

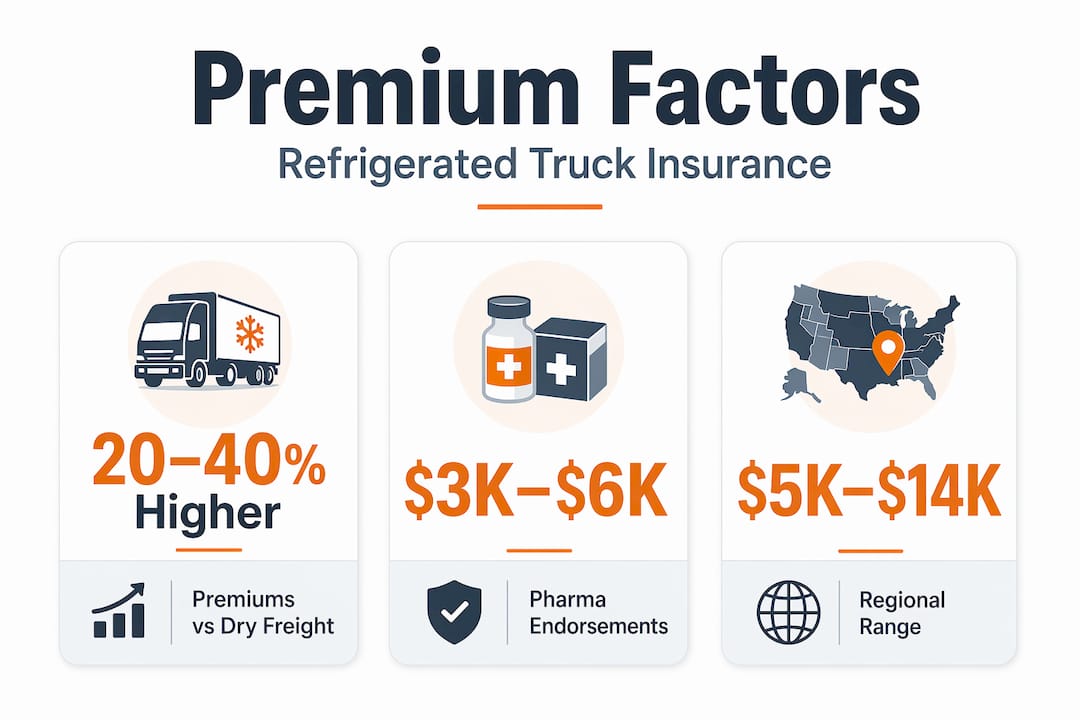

Cargo insurance premiums for refrigerated trucks run 20 to 40% higher than comparable dry freight operations. The reasons are straightforward: higher cargo values, more complex equipment that can fail, and tighter temperature compliance windows that create bigger claims when something goes wrong.

Premium ranges by cargo type and region

Cargo Type | Estimated Annual Premium Range | Key Cost Driver |

Standard frozen foods | $1,500 to $4,000 per truck | Volume, claims history |

Fresh produce | $2,000 to $5,000 per truck | Spoilage sensitivity, transit time |

Pharmaceuticals | $3,000 to $6,000 per unit | Strict compliance, high value |

Florida-based operations | $5,000 to $14,000 per truck | Regional heat exposure |

Pharmaceutical refrigerated transport endorsements can reach $3,000 to $6,000 per unit annually because the compliance requirements are stricter and the cargo values are significantly higher. A single pallet of temperature-sensitive medication can be worth more than some entire dry freight loads. Carriers writing this coverage want to see documented cold chain protocols, validated temperature monitoring, and training records before they price the risk.

Geography matters more than most fleet managers expect. Florida refrigerated truck insurance premiums average $5,000 to $14,000 per truck annually. That range reflects the state’s heat exposure, longer average spoilage windows when a unit fails in summer, and the sheer volume of produce and perishable goods moving through the region. Operating in the Pacific Northwest with mild summers and shorter transit windows looks very different to an underwriter.

What actually moves your premium up or down

Equipment age is a major factor. Older reefer units with higher breakdown histories get priced accordingly. A fleet running newer units with telematics installed, GPS temperature monitoring, and documented maintenance programs is a fundamentally different risk than an aging fleet with paper maintenance logs and no remote monitoring.

Your claims history follows you. Three spoilage claims in two years will push you into a higher-risk tier regardless of how good your current practices are. Conversely, a clean five-year history with documented driver training and maintenance programs can qualify you for preferred rates with specialized carriers.

Pro Tip: Raising your deductible on cargo coverage from $1,000 to $2,500 and reinvesting those savings into a telematics and temperature monitoring system is often a better long-term move. The monitoring reduces claim frequency; the deductible adjustment reduces premium.

Operational practices that protect your coverage

Having the right policy matters less than you might think if your operations cannot support a claim when one occurs. The best cold chain insurance options on the market will still result in denied claims if your documentation is weak or your maintenance program is inconsistent.

Here is the operational framework that keeps both your cargo safe and your coverage intact:

Implement a formal preventive maintenance schedule. Every reefer unit should have a service log that documents inspections, repairs, refrigerant levels, and software updates. The log should be dated, signed, and stored in a format your insurer can access quickly. Documented preventive maintenance programs qualify fleets for preferred insurance rates in addition to reducing actual breakdown frequency.

Install continuous temperature monitoring with automatic alerts. A telematics system that records temperature data at regular intervals creates the evidence trail you need for a successful claim. It also allows your dispatcher to catch a temperature excursion in real time rather than discovering it at delivery. The response window matters enormously for both the cargo and the claim.

Train drivers specifically on reefer operations. General CDL training does not cover what to do when a reefer alarm triggers at 2 a.m. Drivers should know how to check unit status, when to call for emergency service, when to contact dispatch, and how to document everything that happens during an excursion event. FSMA and FDA compliance requirements, including driver training records, are increasingly reviewed by insurers before offering pricing on refrigerated cargo policies.

Create a written emergency response protocol. What happens in the first 30 minutes after a reefer alarm is often what determines whether a claim gets paid. A written protocol that drivers follow consistently creates the documentation trail that supports a defensible claim. This includes timestamped notes, photos, unit error codes, and contact records.

Understand your shipper contracts before you haul. Many refrigerated transport liability issues arise from contract terms that operators have not fully read. If a shipper contract holds you responsible for temperature maintenance from loading to delivery, your insurance needs to match that obligation. Mismatches between contract language and policy language create uncovered losses.

Pro Tip: After any temperature excursion, no matter how minor, build your claims packet the same day. A well-assembled defensible packet including temperature data, maintenance proof, and driver notes significantly increases your probability of claim approval. Waiting a week means lost details and a harder conversation with the adjuster.

Emerging risks that standard policies miss

Getting the foundational coverage right is the starting point. Beyond that, refrigerated trucking operations face a set of evolving risks that even experienced fleet managers have not fully factored into their insurance strategy.

The legal environment is getting more expensive

Nuclear verdicts exceeding $100 million have become a real factor in commercial trucking insurance pricing. These verdicts do not need to involve your fleet directly. When large awards push carriers to tighten terms and raise premiums across the board, every refrigerated trucking company absorbs the impact. Legal rulings that expand broker liability also create new questions about who is responsible when a spoiled load leads to a lawsuit.

This is part of why working with insurers and brokers who specialize in refrigerated transport liability matters more now than it did five years ago. A specialist understands how to structure policies that account for the current legal environment, not just the base coverage requirements.

The cyber and cargo coverage gap

This one catches operators completely off guard. A growing number of refrigerated logistics operations are connected systems. Temperature monitoring runs through software platforms. Load assignments flow through digital freight platforms. Payment and invoice systems are integrated.

When a cyberattack causes cargo loss or invoice manipulation, cargo policies exclude cyber events and cyber policies exclude physical cargo loss. The result is a coverage gap that sits squarely in the middle of how modern refrigerated logistics actually operates. Understanding this gap is the first step toward addressing it, whether through a specialized endorsement, a hybrid policy structure, or explicit policy language from a carrier who acknowledges the overlap.

Common claim documentation pitfalls

Beyond the exclusions in your policy language, the claims process itself creates risk for operators who are not prepared:

Delayed reporting after a temperature excursion can trigger a late-notice exclusion even when the underlying loss is covered.

Missing maintenance logs give adjusters grounds to argue that improper maintenance caused the failure rather than a sudden equipment breakdown.

Poorly documented mitigation steps, such as not attempting to transfer cargo or contact emergency refrigeration services, can reduce the indemnity amount even when the claim is accepted.

Salvage cost disputes arise when insurers and operators disagree on the value of partially affected cargo.

“The difference between a paid claim and a denied claim is often not the policy language. It is the paperwork that exists before the claim is ever filed.” This reflects what verifiable maintenance records and claims history mean to every underwriter reviewing your account.

My honest take on reefer insurance strategy

I have reviewed a lot of refrigerated trucking insurance situations, and the most consistent pattern I see is operators who treat cold chain insurance options as a commodity purchase. They shop for the lowest annual premium, bind coverage without reading the exclusions, and then discover what they actually bought when a claim gets denied.

Here is what I have learned: the reefer breakdown endorsement is not optional, and the difference in cost between a policy with solid exclusion language and one with broad exclusions is rarely more than a few hundred dollars per year. That gap is meaningless compared to a $60,000 spoiled pharmaceutical load that your adjuster declines to pay because you cannot produce a maintenance log from 90 days prior.

The operators who do this well treat their insurance program as a managed asset. They know their exclusions. They keep their documentation current. They run telematics not because the insurer requires it but because it makes their claims defensible and their premiums negotiable. Working with a specialist who understands fleet insurance coverage for reefer operations versus general commercial trucking makes a real difference in how your program is structured and what you actually get when something goes wrong.

The fleet managers I respect most in this space are the ones who can hand their insurer a complete maintenance binder, a telematics report, and a driver training log at renewal. That documentation alone changes the conversation from “what is the minimum we can offer?” to “what rate does this fleet deserve?”

— Guyorguy

Get your reefer insurance organized with Insuaria

Refrigerated trucking operations have more insurance moving parts than almost any other freight category, and getting them organized before talking to a licensed professional makes the entire process faster and less frustrating. Insuaria is a compliance-first intake and referral platform that helps trucking businesses pull together the details licensed insurance professionals need to review your coverage situation.

Through Insuaria’s business insurance intake form, you can organize your fleet details, cargo types, operational regions, and compliance documentation in one place before a licensed agency partner follows up. Insuaria does not bind coverage or make recommendations, but it removes the disorganized first step that slows most fleet managers down. You can also explore Insuaria’s trucking insurance intake to get your information ready for the specialists who handle refrigerated cargo programs.

FAQ

What does reefer breakdown coverage actually cover?

Reefer breakdown coverage pays for cargo losses caused by the sudden and accidental failure of refrigeration equipment during transit. It does not cover losses from operator error, delayed response, or improper maintenance.

Is reefer breakdown insurance required by law?

No federal regulation mandates reefer breakdown coverage, but most shippers and freight brokers require it contractually as a condition of hauling temperature-controlled freight.

How much does insurance for refrigerated trucking cost?

Annual premiums typically range from $1,500 to $14,000 per truck depending on cargo type, operating region, equipment age, and claims history. Pharmaceutical transport and Florida-based operations sit at the higher end of that range.

Why do refrigerated truck insurance premiums run higher than dry freight?

Refrigerated truck insurance runs 20 to 40% higher than dry freight coverage because of higher cargo values, more complex equipment with greater breakdown potential, and tighter temperature compliance windows that increase claim severity.

What documentation do I need to support a refrigerated cargo claim?

Insurers typically require temperature logs, proof of preventive maintenance, driver incident reports, and documented mitigation steps. A complete claims defensible packet assembled promptly after an excursion gives you the strongest position for claim approval.

Recommended

Comments