Understand physical damage coverage for auto and home

- Guyorguy Laguerre

- May 7

- 11 min read

TL;DR:

Most people misunderstand the significance of physical damage coverage, which determines claim payouts and approval. It protects against losses to your property caused by covered events, including collision, comprehensive, and certain home perils, but excludes wear and tear and maintenance issues. Reviewing and documenting your coverage annually helps ensure proper protection, as valuation methods and property values change over time, preventing disputes during claims.

Most people glance at their insurance policy, see the phrase “physical damage coverage,” and assume they understand it. They don’t. This single term shapes how much money you receive after a car accident, a hailstorm, or a break-in, and it determines whether a claim gets approved or disputed. Physical damage coverage is not a vague catch-all. It is one of the most specific and consequential components of both auto and home insurance, and knowing exactly what it means, how payouts are calculated, and what documentation is required can be the difference between a smooth claim and a frustrating one.

Table of Contents

Key Takeaways

Point | Details |

Physical damage coverage basics | This coverage protects your vehicle or home from accidental or peril-based losses. |

Documentation is critical | Submitting accurate records and photos increases claim success and payments. |

Exclusions limit protection | Most policies don’t cover wear-and-tear, maintenance, or some preventable damages. |

Required vs. optional | Lenders and insurers may require coverage, but it’s often optional for owners. |

Smart review saves money | Understanding fine print and preparing in advance avoids unpleasant surprises. |

What is physical damage coverage?

Physical damage coverage protects against covered losses to your vehicle or your home’s physical structure and belongings. In plain terms, it is the part of your policy that pays to repair or replace your property after a qualifying event. This is fundamentally different from liability coverage, which handles injury claims or property damage you cause to someone else. Think of it this way: liability coverage protects others from you, while physical damage coverage protects you from events.

In auto insurance, physical damage coverage is an umbrella term that includes two distinct components.

Collision coverage pays for damage to your vehicle caused by an impact with another car, a fence, a telephone pole, or any other object, regardless of fault.

Comprehensive coverage pays for damage caused by events outside of a collision, including theft, fire, flooding, hail, fallen trees, and vandalism.

Gap coverage is sometimes bundled with physical damage to cover the difference between what your vehicle is worth and what you still owe on a loan.

In home insurance, the concept works similarly but under different labels. Nolo describes standard homeowners insurance as including a hazard or physical damage component that pays for damage to your home and belongings from covered perils. This is typically structured as Coverage A (dwelling), Coverage B (other structures), and Coverage C (personal property). The liability portion of your homeowners policy is entirely separate, covering third-party injury or property damage claims against you.

Physical damage coverage in auto insurance pays for what happens to your car. In home insurance, it pays for what happens to your house and belongings. Both are distinct from liability coverage types, which cover claims made by others.

Understanding the difference between liability vs. physical damage is the foundation for reviewing any insurance policy. Many families focus so much on liability limits that they overlook whether their physical damage coverage actually reflects the current value of their home or vehicle. That oversight can cost thousands.

How physical damage coverage works: Payouts, deductibles, and documentation

With a clear definition in mind, it is essential to understand how actual payments are calculated, and what documentation is needed when a claim happens.

The payout formula is straightforward on paper but complicated in practice. Documentation and valuation disputes can lead to lower-than-expected claim payouts when the insurer uses actual cash value (ACV) instead of replacement cost. Here is how each method differs:

Valuation method | What it means | Best for |

Actual cash value (ACV) | Pays what your property is worth today, after depreciation | Older vehicles or homes |

Replacement cost value (RCV) | Pays what it costs to replace with a comparable new item | Newer vehicles or upgraded homes |

Agreed value | A pre-determined payout amount agreed upon at policy start | Specialty or classic vehicles |

The deductible, which is the amount you pay out of pocket before coverage kicks in, directly reduces your payout. If your car sustains $6,000 in damage and your deductible is $1,000, the insurer pays $5,000. If ACV is used and your vehicle has depreciated, that payout could shrink further. Choosing a higher deductible lowers your premium, but it also increases your financial exposure at claim time. Understanding how deductibles impact payouts before you set your policy is one of the most practical moves you can make.

Documentation required for a physical damage claim:

Proof of ownership for vehicles: title, registration, or loan documents; for homes: deed or mortgage statement.

Evidence of the loss: police reports for theft or vandalism, weather records for storm damage, photos and video taken immediately after the event.

Damage assessment: a written estimate from a licensed repair shop or contractor, or an independent appraisal.

Receipts and records: purchase receipts, renovation permits, and home improvement records that demonstrate the value of what was lost.

Prior inspection records: maintenance logs for vehicles, and inspection or appraisal records for homes, to establish condition before the loss.

Pro Tip: Take a full photo and video walkthrough of your home’s interior and exterior at least once a year, and store it in a cloud folder. Do the same for your vehicle. These records are inexpensive to create and invaluable during a dispute over valuation.

One of the most common reasons claims are disputed is incomplete documentation. The insurer needs to verify what existed, what it was worth, and how the damage occurred. If you cannot provide photos or receipts, the insurer may estimate conservatively, and that estimate tends to favor the insurer, not you. According to industry surveys, a significant percentage of homeowners who filed claims reported receiving less than they expected, often because they lacked receipts or photos documenting the condition of damaged items.

Why ACV vs. replacement cost matters more than you think. Imagine your five-year-old laptop is stolen from your home. Under ACV, you might receive $300 because that is what a five-year-old laptop is worth today. Under replacement cost, you could receive $900 because that is what a comparable new model costs. That $600 gap is real money, and it is determined entirely by which valuation method your policy uses.

When is physical damage coverage required or optional?

After understanding payouts, deductibles, and documentation, it is important to recognize where coverage is mandatory, and what happens if it is omitted.

For auto insurance, physical damage is commonly required by lenders and lease agreements. If you financed or leased your vehicle, your lender or lessor has a financial interest in that asset and will require both collision and comprehensive coverage until the loan is paid off or the lease ends. Once you own the vehicle outright, physical damage coverage becomes optional, though that does not necessarily mean you should drop it.

For homeowners, mortgage lenders typically require hazard insurance, which is the home equivalent of physical damage coverage. This requirement protects the lender’s collateral in case the property is destroyed or severely damaged. If you allow your hazard coverage to lapse while carrying a mortgage, the lender can purchase a policy on your behalf, known as force-placed insurance, and charge you for it. Force-placed policies are almost always more expensive and provide less protection than policies you choose yourself.

Situation | Physical damage coverage status |

Financed or leased vehicle | Required by lender or lessor |

Owned vehicle (paid off) | Optional, based on vehicle value and risk |

Home with active mortgage | Required by lender (hazard insurance) |

Home owned outright | Optional, strongly recommended |

Rental property | May be required by mortgage terms |

Commercial vehicle requirements add another layer of complexity for business owners operating vehicles commercially.

Insurance requirements tips for fleet operators can also inform how individuals think about personal coverage thresholds.

Lenders typically require you to name them as a “loss payee” on the policy, meaning the insurer issues claim payments jointly or directly to the lender.

Optional coverage decisions should factor in the current market value of the vehicle or property, not just the original purchase price.

Pro Tip: If your vehicle’s market value has dropped significantly, compare your annual collision and comprehensive premium against the vehicle’s actual cash value. If the premium equals or exceeds 10% of the vehicle’s value, you may want to discuss whether continued coverage makes financial sense with a licensed insurance professional.

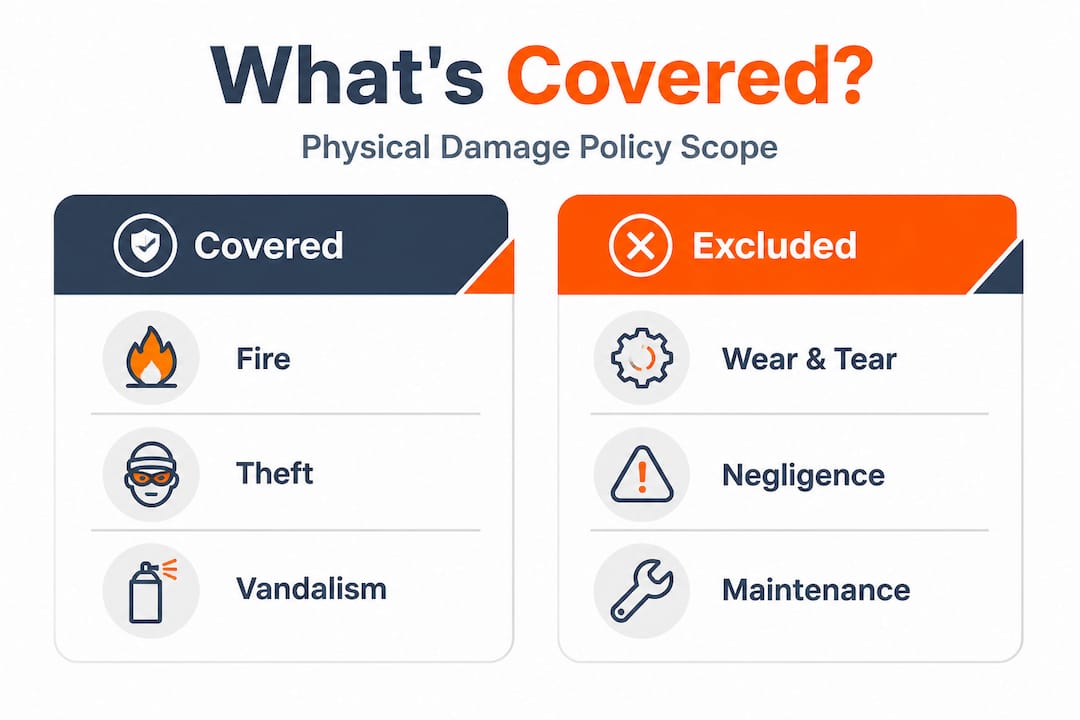

One frequently overlooked exclusion in every physical damage policy is damage caused by normal wear and tear or lack of maintenance. Your engine failing after 200,000 miles is not a covered physical damage event. Rust that slowly eats through your car’s body is not covered. A roof that deteriorates over decades without maintenance is not covered by your homeowners policy either. These exclusions are written into every standard policy, but many people do not discover them until after a claim is denied.

Physical damage coverage exclusions and common pitfalls

Having established requirements, let’s turn to what is not covered, the exclusions and common pitfalls that may surprise policyholders.

Every physical damage policy has a list of exclusions, events or conditions that the insurer will not pay for. Policies typically exclude wear and tear and maintenance-related damage as a standard provision. But the exclusion list goes further than most people realize.

Common exclusions in physical damage policies:

Wear and tear: Gradual deterioration from normal use is never covered.

Mechanical or electrical failure: A blown engine or failing transmission is a mechanical issue, not a covered physical damage event unless caused by a covered accident.

Preventable damage: If you fail to take reasonable steps to prevent further damage after a covered loss, such as leaving a vehicle with a broken window in a rainstorm, the insurer can reduce or deny payment for the additional damage.

Intentional acts: Damage you cause deliberately to your own property is excluded.

Flood damage (standard auto policy): Standard auto policies typically exclude flood unless you have comprehensive coverage.

Earthquake (standard home policy): Most standard homeowners policies exclude earthquakes; separate coverage must be purchased.

Mold and pest infestations: These are considered preventable maintenance issues.

“If you don’t take reasonable steps to prevent further damage after a loss, the insurer may reduce your payout or deny the additional damage claim entirely.”

The preventable damage pitfall catches many policyholders off guard. Imagine a tree falls on your car during a storm. The initial impact is covered. But if you leave the car exposed with a shattered windshield for two weeks during a rain period, the water damage that accumulates may not be covered because you had the opportunity to cover or move the vehicle and did not. The same logic applies to home damage. A pipe bursts, you see water damage beginning to form, but you wait several days to call a contractor. The insurer may only cover the original pipe damage, not the mold that developed because you delayed action.

Insurance exclusions confidence comes from reading and understanding the exclusions section of your policy before any loss occurs, not after. It is a section most people skip entirely, which is exactly why claim disputes are so common.

Another common pitfall is confusing “named perils” policies with “open perils” policies. A named perils policy only covers events specifically listed, such as fire, theft, and wind. An open perils policy, also called all-risk, covers everything except what is specifically excluded. Open perils policies tend to cost more but offer broader protection. Knowing which type of policy you have changes how you interpret your coverage significantly.

The documentation pitfall. Many families assume that if they paid for something, the insurer will cover it. But without documentation, that assumption means nothing in a claim dispute. A luxury appliance, a custom renovation, a recently purchased bicycle. If you cannot prove what it cost and what condition it was in, the insurer’s adjuster will estimate, and those estimates tend to be conservative. Build your documentation habit before you need it.

Our take: Why smart policyholders look beyond basic coverage

All the facts and tables aside, here is what we believe really matters when choosing physical damage coverage for your family or home.

The conventional wisdom is that meeting the minimum coverage requirement is good enough. If your lender requires collision and comprehensive, you buy it. If the mortgage company wants hazard insurance, you get the cheapest policy that satisfies the requirement. Done. The problem with that approach is that meeting the minimum does not mean you are actually protected. It means you have satisfied someone else’s requirement, not your own financial interest.

Seasoned insurance reviewers, and the families who have been through a major claim, know that the real work happens before any loss occurs. They ask specific questions: Does my policy use ACV or replacement cost? What is the exact deductible for hail versus collision? Which perils are named, and which are excluded? These are not difficult questions, but most people never think to ask them until after a claim goes sideways.

There is also a documentation gap that affects nearly every family we see come through the insurance review process. People spend years accumulating furniture, electronics, tools, clothing, and home improvements, but they never take stock of what they own or what it is worth. When a fire or theft occurs, they are left trying to reconstruct years of purchases from memory while already dealing with the stress of a loss. That is an avoidable situation.

Fleet managers in the commercial trucking world learned this lesson years ago. They maintain detailed vehicle records, keep maintenance logs, and document every upgrade. They do this not because they enjoy paperwork, but because they have seen firsthand what happens when a claim lacks supporting documentation. Individuals and families can apply that same discipline at home. It does not require complex software. A folder on your phone with dated photos and scanned receipts is enough.

We also believe that the smartest move any policyholder can make is to review their physical damage coverage annually. Values change. A vehicle you bought five years ago at $35,000 might be worth $18,000 today. Carrying a $2,000 annual premium for physical damage coverage on an $18,000 vehicle may or may not make sense, depending on your risk tolerance and financial cushion. The strategies that help people reduce insurance premiums in commercial settings translate directly to personal auto and home decisions. Review your values, update your documentation, and ask your licensed insurance professional whether your current coverage structure still fits your situation.

Simplify your insurance review with Insuaria

Understanding physical damage coverage is one thing. Having the right documentation organized and ready for a licensed insurance professional to review is another step entirely.

Insuaria makes that second step easier. Through a simple auto insurance review intake form, you can organize the vehicle details and coverage information that a licensed agency partner may need to evaluate your current auto coverage. If you are reviewing your homeowners policy, the home insurance review intake process guides you through the property and coverage details that matter most. And when it comes to documentation, the insurance document upload tool lets you submit photos, receipts, and policy documents securely in one place. Insuaria does not provide coverage advice or issue quotes, but it does make sure the right information is organized and ready when a licensed professional follows up.

Frequently asked questions

Is physical damage coverage the same as collision or comprehensive coverage?

Physical damage coverage includes both collision and comprehensive. Collision covers accidents involving other vehicles or objects, while comprehensive covers non-collision events like theft, fire, or hail, and claim payouts depend on your deductible and valuation method.

Do I need physical damage coverage if I own my car outright?

Physical damage coverage is optional for outright owners, but lenders commonly require it when financing or leasing. It may still be recommended for higher-value vehicles or when out-of-pocket repair costs would create a financial hardship.

What documentation is required to file a physical damage claim?

You need proof of ownership, photos of the damage, a repair or replacement estimate, and receipts for the damaged property. Valuation disputes frequently arise when documentation is incomplete, often resulting in lower payouts than expected.

Are maintenance issues covered by physical damage policies?

No. Wear-and-tear and maintenance damage are standard exclusions in physical damage policies, for both auto and home coverage. These are considered preventable conditions, not sudden covered losses.

How does a deductible affect my claim payout?

Your deductible is subtracted from the covered loss before the insurer pays. If you have a $1,500 deductible and a $5,000 covered loss, the insurer pays $3,500, regardless of which valuation method applies.

Recommended

Comments