What Is Umbrella Trucking Insurance for Fleets?

- Guyorguy Laguerre

- 4 days ago

- 10 min read

TL;DR:

Umbrella trucking insurance acts as a supplemental liability policy that activates after primary policy limits are exhausted, protecting fleets from catastrophic financial losses. It offers broader, gap-filling coverage and is essential for securing major contracts, with premiums scaled to fleet size and risk. Fleet owners should purchase it proactively before negotiations to ensure coverage adequacy and compliance.

Umbrella trucking insurance is a supplemental liability policy that activates after your primary commercial auto or general liability coverage reaches its limits, shielding your fleet from catastrophic financial losses that a standard policy cannot absorb. Known formally as a commercial trucking umbrella policy, this coverage sits above your underlying policies and pays claims that would otherwise come directly out of your business assets. For fleet owners operating in 2026, where a single serious accident can generate multi-million-dollar lawsuits, understanding what umbrella trucking insurance covers is not optional. It is the difference between a recoverable loss and a business-ending judgment.

What is umbrella trucking insurance and how does it work?

A commercial trucking umbrella policy is structured in layers. Your primary policies, typically commercial auto liability and general liability, form the foundation. Once a covered claim exhausts those underlying limits, the umbrella policy takes over and pays the remaining balance up to its own limit. This layered structure is why umbrella coverage provides a financial safety net above primary policies, covering catastrophic losses that can bankrupt a business.

The attachment point is the threshold at which the umbrella kicks in. For most trucking operations, that attachment point matches the limit of the primary policy, often $1 million. If a jury awards $3.5 million in a collision case and your primary auto liability limit is $1 million, the umbrella covers the remaining $2.5 million. Without it, your fleet, equipment, and operating capital are exposed.

Umbrella policies tailored for trucking operations go beyond simple overflow protection. They can include regulatory action defense funding, third-party injury indemnity, and completed operations coverage, making them far more versatile than most fleet owners realize. This breadth is what separates a well-structured trucking umbrella from a basic excess liability add-on.

Pro Tip: Review your primary policy’s attachment point language before purchasing an umbrella. If your primary policy has a sublimit for certain cargo types, your umbrella may not attach until that sublimit is exhausted, not the full policy limit.

What coverage limits and costs should fleet owners expect?

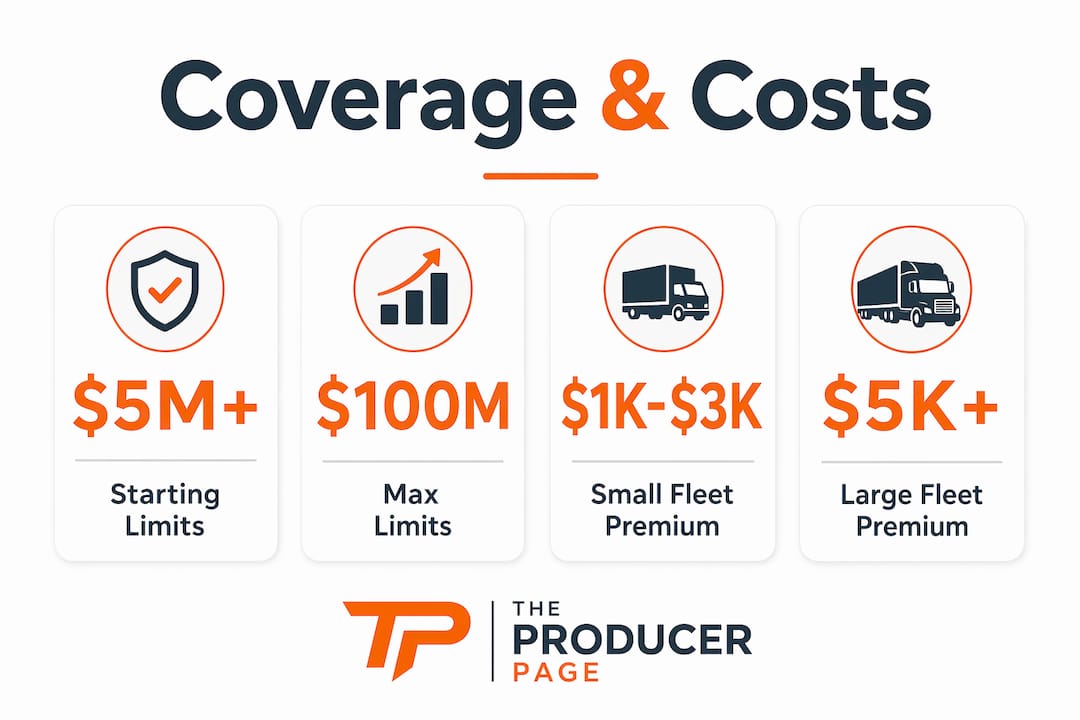

Coverage limits for umbrella trucking insurance start at $5 million and can reach $100 million or more for large fleets carrying high-value or hazardous cargo. That range reflects the enormous variation in risk exposure across the trucking industry. A three-truck regional carrier hauling dry goods faces a fundamentally different risk profile than a 50-truck fleet moving temperature-sensitive pharmaceuticals across state lines.

Premiums follow a similar range. Small fleets typically pay between $1,000 and $3,000 annually for umbrella coverage, while mid-size operations can expect $10,000 or more depending on fleet size, cargo type, and claims history. The table below outlines typical limit and cost ranges by fleet size.

Fleet size | Typical umbrella limit | Estimated annual premium |

1 to 5 trucks | $5M to $10M | $1,000 to $3,000 |

6 to 20 trucks | $10M to $25M | $3,000 to $7,000 |

21 to 50 trucks | $25M to $50M | $7,000 to $10,000+ |

50+ trucks | $50M to $100M+ | $10,000 to $25,000+ |

These figures are general benchmarks. Underwriters weigh your loss runs, driver records, operating radius, and cargo class before finalizing a premium. A fleet with clean loss history and verified safety programs will consistently pay less than one with frequent claims, even at the same size.

The relationship between premium cost and risk tolerance is direct. Paying $5,000 annually for a $25 million umbrella limit costs less than a single uninsured judgment of $2 million. Viewed as a cost-per-unit-of-protection calculation, umbrella coverage is among the most efficient purchases in the trucking insurance options available to fleet operators.

Pro Tip: Ask your broker for a “schedule of underlying insurance” review before binding an umbrella. Gaps or mismatches between your primary policies and the umbrella’s required underlying limits can void coverage at the worst possible moment.

How umbrella insurance differs from excess liability coverage

Most fleet owners treat umbrella and excess liability as interchangeable terms. They are not. Umbrella coverage typically offers broader protection beyond simply adding limits, while excess liability strictly layers additional limits on top of a single underlying policy without expanding coverage scope.

The practical difference matters when a claim falls into a gap between your underlying policies. An umbrella policy, particularly one written on a “follow-form” basis with gap-filling provisions, can step in to cover that claim. An excess liability policy will not. It only responds to claims that the underlying policy would have covered, just at a higher dollar amount.

Feature | Umbrella policy | Excess liability policy |

Coverage scope | Broader, fills gaps between underlying policies | Mirrors underlying policy only |

Gap coverage | Yes, can cover uncovered claims | No |

Policy form | Follow-form with enhancements | Strictly follow-form |

Shipper preference | Preferred for multi-policy operations | Acceptable for single-policy stacking |

Best suited for | Fleets with multiple underlying policies | Fleets seeking simple limit increases |

Shippers prefer umbrella coverage for multi-policy operations because it provides more predictable protection across complex risk profiles. A carrier with commercial auto, general liability, and motor truck cargo policies benefits more from an umbrella that coordinates across all three than from an excess policy tied to just one.

Prudent fleet owners prefer umbrella policies that follow form but complement underlying policies, minimizing coverage gaps rather than simply increasing limits. This distinction is worth discussing explicitly with your broker, because not all policies marketed as “umbrella” actually provide gap-filling coverage.

Pro Tip: Request the policy’s “other insurance” clause in writing. This clause defines how the umbrella interacts with your underlying policies and determines whether gaps are actually covered or just assumed to be.

Why umbrella coverage is critical for contracts and compliance

The Federal Motor Carrier Safety Administration sets minimum liability thresholds: $750,000 for general freight, $1 million for oil transport, and $5 million for hazardous materials. These federal floors are the legal minimum. They are not what major shippers, retailers, or government agencies actually require before tendering loads.

Shippers frequently demand $1 million or more in primary liability coverage and $2 million to $5 million in umbrella coverage before a carrier can haul their freight. This is not a suggestion. It is a contract condition. Umbrella insurance is often required to secure contracts with major retailers and government agencies that mandate higher liability limits. Carriers without adequate umbrella coverage simply cannot access those lanes.

The compliance requirements that fleet owners need to track include:

Federal minimums: FMCSA mandates $750,000 to $5 million depending on cargo type. These are the floor, not the ceiling.

Shipper contract requirements: Most Fortune 500 shippers and third-party logistics providers require $2 million to $5 million in umbrella or excess liability coverage.

Broker requirements: Many freight brokers include insurance minimums in their carrier agreements, and non-compliance disqualifies a carrier from their load board.

State-specific mandates: Several states impose additional liability requirements for intrastate operations that exceed federal minimums.

Government contracts: Federal and state agency freight contracts routinely require $5 million or more in total liability coverage, making umbrella coverage a prerequisite.

Operators who wait for last-minute coverage risk underwriting delays and increased premiums. Securing umbrella coverage before contract negotiations begin, not after a shipper requests a certificate of insurance, gives your fleet negotiating leverage and avoids emergency placements that cost more and deliver less.

How umbrella insurance manages litigation and defense costs

Legal defense costs in trucking are not a minor line item. Defense costs average $35,000 to $75,000 per claim, and total uncovered expenses can reach $50,000 to $200,000 or more without adequate umbrella coverage. A single serious accident involving injuries, cargo damage, and property destruction can generate multiple simultaneous claims, each carrying its own defense costs.

The structure of your umbrella policy’s defense cost provision determines how much protection you actually have. The critical distinction is whether defense costs are paid “inside” or “outside” the policy limit.

Inside limits: Defense costs reduce the available coverage limit. A $5 million umbrella policy that pays $1.5 million in defense costs leaves only $3.5 million for settlements and judgments.

Outside limits: Defense costs are paid separately, preserving the full $5 million limit for settlements. This structure provides significantly more net protection.

Duty to defend: Some umbrella policies include a duty to defend, meaning the insurer controls and funds the legal defense. Others are indemnity-only, meaning you fund the defense and seek reimbursement.

Reservation of rights: Understand when your insurer can defend under a reservation of rights, which signals a potential coverage dispute even while the defense is active.

Coordination with primary defense: When both primary and umbrella insurers are involved, defense coordination agreements prevent conflicting legal strategies that can harm your case.

If defense costs are inside the coverage limit, a major claim can exhaust umbrella limits on defense alone, leaving nothing for the actual settlement. Insurers and brokers consistently recommend outside-limit defense coverage to preserve available limits for judgments. This single policy feature can mean the difference between a covered loss and a personally devastating financial outcome for fleet owners. Understanding why trucking insurance costs what it does starts with recognizing how much litigation exposure drives underwriting decisions.

Practical tips for choosing umbrella trucking insurance in 2026

Selecting the right commercial trucking umbrella policy requires more than picking a limit and signing a binder. The following steps help fleet owners structure coverage that actually performs when a major claim occurs.

Assess your true risk exposure. Map your fleet size, cargo types, operating regions, and average load values before approaching underwriters. A fleet hauling construction equipment through mountain corridors carries more catastrophic loss potential than one delivering packaged goods on urban routes. Your limit selection should reflect actual exposure, not industry averages.

Verify your primary policies meet attachment point requirements. Umbrella underwriters specify minimum underlying limits before they will write coverage. If your commercial auto policy carries a $500,000 limit but the umbrella requires $1 million as an attachment point, you have a gap. Confirm all underlying policies meet the umbrella’s required minimums before binding.

Request outside-limit defense cost coverage. This is not a standard feature on every policy. Ask specifically for defense costs to be paid outside the limit of liability. The additional premium is modest compared to the protection it provides in complex, multi-party litigation.

Purchase umbrella coverage before contract negotiations, not after. Waiting until after contract signing leads to costly emergency placements or contract non-fulfillment. Carriers who carry umbrella coverage before approaching shippers negotiate from a position of strength.

Review the policy’s “follow-form” provisions carefully. A true umbrella policy should fill gaps between underlying policies. Ask your broker to walk through a hypothetical multi-policy claim scenario to confirm how the umbrella responds when coverage overlaps or gaps exist.

Coordinate renewal dates. Aligning your umbrella renewal with your primary policy renewals prevents coverage gaps during the transition period. Misaligned renewals create windows where the umbrella may not have valid underlying coverage to attach to.

Work with a broker who specializes in commercial trucking. General commercial lines brokers often lack the underwriting relationships and market knowledge to place trucking umbrella coverage competitively. A specialized trucking insurance broker accesses markets that standard brokers cannot reach.

Key takeaways

A commercial trucking umbrella policy is the single most cost-efficient tool fleet owners have to protect business assets from catastrophic liability claims, litigation costs, and contract disqualification.

Point | Details |

Coverage structure | Umbrella activates after primary policy limits are exhausted, covering remaining claim amounts. |

Cost efficiency | Premiums range from $1,000 to $10,000+ annually, far less than a single uncovered judgment. |

Umbrella vs. excess | Umbrella fills coverage gaps; excess liability only adds limits to a single underlying policy. |

Contract compliance | Major shippers and government agencies require $2M to $5M umbrella coverage before tendering loads. |

Defense cost structure | Outside-limit defense coverage preserves full policy limits for settlements rather than legal fees. |

Why fleet owners underestimate umbrella insurance until it’s too late

I have reviewed hundreds of trucking insurance portfolios over the years, and the pattern is consistent. Fleet owners who have never filed a catastrophic claim treat umbrella coverage as an optional upgrade. Fleet owners who have faced a serious multi-party accident treat it as the most important policy they carry.

The misconception I encounter most often is that $1 million in primary auto liability is sufficient for a professional carrier. It was barely adequate a decade ago. Today, nuclear verdicts in trucking cases regularly exceed $10 million, driven by aggressive plaintiff attorneys who specifically target commercial carriers because juries perceive them as deep-pocketed defendants. A $1 million primary policy is not a shield in that environment. It is a starting point.

What I find genuinely underappreciated is the contract access angle. Umbrella insurance enables carrier growth by unlocking contracts that require proof of high-limit liability protection. I have seen small carriers win dedicated shipper contracts worth $500,000 annually simply because they carried $5 million in umbrella coverage and their competitors did not. The premium cost of that umbrella was under $3,000. The return on that investment is difficult to argue against.

The other point worth making directly: do not let your broker default to excess liability when you ask for umbrella coverage. They are not the same product. If your broker cannot explain the gap-filling distinction clearly, find one who can. The essential fleet coverages your operation needs deserve a broker who understands the difference.

— Guyorguy

Get your fleet’s umbrella coverage organized with Insuaria

Structuring umbrella trucking insurance correctly requires organized information before a licensed professional can evaluate your options.

Insuaria is a compliance-first intake and referral platform built specifically to help trucking businesses organize the details licensed insurance professionals need to review coverage. Through a simple business insurance intake form, fleet operators can submit fleet size, cargo types, operating regions, and current coverage details so that a licensed agency partner can follow up with appropriate options. Insuaria does not provide insurance advice, bind coverage, or issue quotes. Every coverage decision is handled by licensed professionals. If you want to stop guessing about whether your umbrella limits are adequate and start getting answers from someone qualified to give them, Insuaria makes that first step straightforward.

FAQ

What is umbrella trucking insurance in simple terms?

Umbrella trucking insurance is a liability policy that pays claims exceeding your primary commercial auto or general liability limits. It activates after your underlying coverage is exhausted and protects your fleet assets from catastrophic losses.

How much umbrella coverage does a trucking fleet need?

Coverage limits typically start at $5 million and scale based on fleet size, cargo type, and contract requirements. Many shippers require $2 million to $5 million in umbrella coverage before tendering loads, making that range a practical minimum for carriers pursuing major contracts.

What is the difference between umbrella and excess liability for truckers?

Umbrella insurance provides broader coverage that can fill gaps between underlying policies, while excess liability strictly adds limits to a single underlying policy without expanding coverage scope. Shippers generally prefer umbrella policies for multi-policy trucking operations.

Does umbrella trucking insurance cover legal defense costs?

It depends on the policy structure. Policies with outside-limit defense coverage pay legal fees separately, preserving the full limit for settlements. Policies with inside-limit defense reduce available coverage as defense costs accumulate, which can leave insufficient funds for judgments.

When should a fleet owner purchase umbrella trucking insurance?

Purchase umbrella coverage before entering contract negotiations with shippers or brokers, not after. Waiting until a contract requires proof of coverage leads to emergency placements that cost more and may not meet underwriting standards in time to fulfill the agreement.

Recommended

Comments