Why Insurance Compliance Is Important for Your Protection

- Guyorguy Laguerre

- 2 days ago

- 9 min read

TL;DR:

Insurance compliance ensures insurers operate legally, maintain financial stability, and treat policyholders fairly.

It directly protects policyholders from claim delays, unfair treatment, and insurer insolvency by enforcing timely payments and solvency standards.

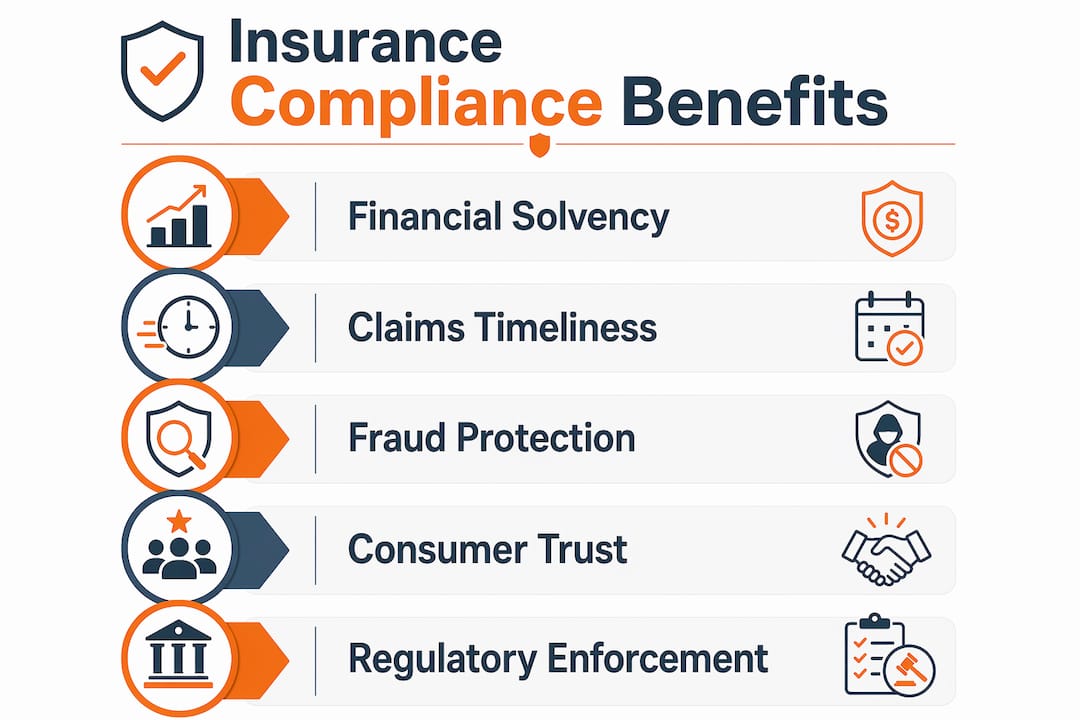

Insurance compliance is the set of rules and practices that require insurance companies to operate legally, maintain financial stability, and treat policyholders fairly. For homeowners, families, and business owners, understanding why insurance compliance is important is not an abstract exercise. It determines whether your insurer can actually pay your claim, whether you are protected from deceptive practices, and whether the coverage you purchased delivers on its promise. Noncompliance triggers fines, license revocations, and lawsuits that ultimately harm the policyholders those insurers are supposed to serve.

Why insurance compliance is important for policyholders

Insurance compliance is not mere paperwork. It is the mechanism that reduces the risk of claim nonpayment, delays, and unfair treatment that would otherwise leave you financially exposed at the worst possible moment. State insurance departments and federal regulations form a layered framework that governs everything from how quickly your insurer must acknowledge a claim to how much capital it must hold in reserve.

When an insurer follows these rules, you benefit directly. Your claim gets processed on a defined timeline. Your insurer cannot arbitrarily deny coverage without documented justification. Your personal data is handled under specific privacy standards. When an insurer ignores these rules, the consequences fall on you: delayed payments, denied claims, and in the worst cases, an insurer that cannot pay at all.

The compliance in insurance industry framework covers three core areas: financial solvency, market conduct, and consumer data protection. Each area addresses a distinct way that an insurer could fail you. Together, they form the foundation of a trustworthy insurance market.

How compliance protects you from claim delays and unfair treatment

Market conduct examinations are the primary tool regulators use to evaluate whether insurers and their agents treat policyholders fairly. Market conduct exams assess insurer and producer treatment of policyholders across claims handling, underwriting, and sales practices. When examiners find problems, regulators issue corrective action plans, fines, and in serious cases, license suspensions.

The practical impact on your claim is significant. Here is how regulated claims timelines work in practice:

Acknowledgment deadline. Many states require insurers to acknowledge a claim within a set number of business days. Texas Insurance Code Chapter 542 sets a 15-business-day window for acknowledgment, acceptance, or denial of a claim.

Payment deadline. Once a claim is accepted, payment must follow within a defined period. Under Texas law, the insurer has 5 business days to issue payment after acceptance.

Penalty for missing deadlines. Texas law imposes 18% annual penalty interest plus attorney fees when insurers miss these deadlines. That financial consequence gives insurers a direct incentive to pay on time.

Rebuttal window in exams. When regulators draft a market conduct report, insurers typically receive around 30 days to respond. How an insurer handles that window reveals the quality of its compliance program.

Enforcement outcomes. Failures identified in market conduct exams lead to corrective plans, fines, and in repeat cases, license revocation. Each of those outcomes affects the insurer’s ability to serve you.

For homeowners filing a property damage claim or business owners seeking payment after a covered loss, these timelines are not bureaucratic details. They are the difference between rebuilding quickly and waiting months while your insurer stalls.

Pro Tip: Before purchasing a policy, check your state insurance department’s website for any enforcement actions filed against the insurer. A pattern of market conduct violations is a reliable signal of future claims problems.

Does insurer solvency compliance protect your assets?

Solvency compliance is the most fundamental layer of insurance regulation, and it protects something specific: the insurer’s ability to pay your claim when the time comes. Solvency standards are the most fundamental compliance measure ensuring an insurer can meet its financial obligations to policyholders.

State insurance departments do not wait for an insurer to collapse before acting. They use a sliding scale of intervention, monitoring financial ratios and capital levels continuously. When an insurer’s numbers deteriorate, regulators step in early with corrective orders, restrictions on new business, or supervised rehabilitation. This proactive approach is what separates regulated insurance markets from unregulated financial products.

Here is what solvency compliance means for you as a policyholder:

Reserve requirements. Insurers must hold capital reserves proportional to their risk exposure. These reserves exist specifically to pay claims, not to fund operations or dividends.

Risk-based capital standards. The National Association of Insurance Commissioners (NAIC) sets risk-based capital formulas that regulators use to flag financially stressed insurers before they become insolvent.

Early intervention authority. Regulators can place an insurer under supervision, restrict its ability to write new policies, or force a merger before policyholders are harmed.

Guaranty association backstop. If an insurer does become insolvent, state guaranty associations provide a safety net. However, coverage caps range from $250,000 to $500,000 depending on the state and product type. That cap may not cover a large commercial claim or a high-value home.

The guaranty association limit is the detail most policyholders never consider until it is too late. A business owner with a $1.2 million commercial property claim against an insolvent insurer may recover only a fraction of that loss. This is precisely why compliance that preserves insurer solvency matters more than the safety net that exists when it fails.

How compliance reduces fraud, protects your data, and builds trust

Insurance fraud costs the industry billions of dollars annually, and those costs are passed directly to policyholders through higher premiums. Compliance programs that address Anti-Money Laundering (AML) standards and consumer data protection are not just regulatory requirements. They are the controls that keep fraud from eroding the value of your coverage.

Unit21 and Focal tie compliance directly to AML standards and consumer data protection, identifying these as core pillars of a sound insurance compliance program. Insurers operating under these standards must screen transactions for suspicious activity, maintain audit trails, and report certain financial patterns to regulators. That discipline makes it harder for bad actors to use insurance products to move illicit funds, which protects the integrity of the entire market.

For homeowners and families, the data protection dimension is equally direct:

Personal information security. Your policy application contains sensitive financial and health data. Compliance with state privacy laws and federal standards like the Gramm-Leach-Bliley Act governs how that data is stored and shared.

Fraud detection controls. Compliant insurers maintain systems to detect fraudulent claims, which protects honest policyholders from bearing the cost of fraud through premium increases.

Distribution channel oversight. Operational risk tied to noncompliance in distribution channels increases when producers lack valid licenses or when errors and omissions coverage lapses. That gap creates liability exposure that can affect how your claim is handled.

Pro Tip: Ask your insurance agent directly whether they carry current errors and omissions coverage. A licensed agent with active E&O coverage is a sign of a professionally managed distribution channel, which reduces your risk of compliance-related claim problems.

A strong compliance culture at an insurer signals something beyond rule-following. It signals that the organization has built systems to catch problems before they reach you. That is the practical benefit of choosing an insurer with a documented compliance program over one that treats regulation as an obstacle.

What enforcement actions mean for you as an insured party

Regulatory enforcement is the mechanism that gives compliance rules their teeth. Understanding how enforcement works helps you evaluate the insurers you choose and recognize warning signs before you are locked into a policy.

The table below compares the main types of enforcement actions regulators use and what each one means for policyholders:

Enforcement action | What it means for policyholders |

Monetary fines | Insurer pays penalties for violations; signals past misconduct worth researching |

Corrective action plan | Insurer must fix identified problems under regulator supervision; ongoing monitoring |

License suspension | Insurer cannot write new policies in the state; existing policyholders may face service disruptions |

License revocation | Insurer loses authority to operate; policyholders transferred or covered by guaranty association |

Lawsuit or consent order | Formal legal action; often involves restitution to harmed policyholders |

Record retention is one of the most overlooked compliance requirements, yet it directly affects enforcement outcomes. NAIC Model #910 sets baseline retention timeframes at the current year plus three years as a minimum. Insurers that destroy records too early cannot respond to regulator data calls, which triggers penalties and undermines their defense in market conduct exams.

For you as a policyholder, an insurer with strong record retention practices is an insurer that can document its handling of your claim if a dispute arises. That documentation is your protection in a coverage dispute or bad faith lawsuit. Treating a market conduct exam rebuttal as a litigation-grade evidence exercise, as experienced compliance professionals recommend, reflects the seriousness with which well-run insurers approach their obligations to you.

Business owners who rely on fleet insurance compliance understand this dynamic well. A single enforcement action against a carrier can disrupt an entire fleet’s coverage, creating operational and financial exposure that far exceeds the cost of maintaining compliance from the start.

Key takeaways

Insurance compliance protects policyholders by enforcing solvency standards, fair claims handling, fraud prevention, and regulatory accountability that together determine whether your coverage actually pays when you need it.

Point | Details |

Compliance enforces claim timelines | States like Texas impose 18% penalty interest on insurers that miss payment deadlines, giving you legal recourse. |

Solvency rules protect your claim payment | Regulators intervene before insurer collapse, but guaranty association caps mean compliance is your best protection. |

Fraud and data controls benefit policyholders | AML and privacy compliance reduce fraud costs and protect your sensitive personal information. |

Enforcement actions signal insurer quality | Checking your state department’s enforcement history reveals patterns of misconduct before you buy a policy. |

Record retention affects your claim disputes | Insurers with strong retention practices can document their handling of your claim, protecting you in disputes. |

Why I think most people misunderstand what compliance actually does for them

Most homeowners and business owners think of insurance compliance as something that happens inside an insurer’s legal department, completely separate from their experience as a policyholder. That framing is wrong, and it costs people money.

I have seen the pattern repeatedly. A homeowner files a water damage claim and waits three months for a response. A business owner gets a coverage denial with no documented justification. In both cases, the underlying problem traces back to an insurer with a weak compliance culture, one that treats regulatory requirements as minimum thresholds rather than operational standards.

The uncomfortable truth is that compliance is the only thing standing between you and an insurer that delays, denies, and disputes every claim. When regulators enforce prompt payment laws, conduct market exams, and monitor solvency ratios, they are doing the work that most policyholders do not know they need done on their behalf.

What I find most underappreciated is the solvency piece. People buy insurance from a carrier because the premium is competitive, without ever checking whether that carrier has the capital to pay a large claim. The guaranty association backstop sounds reassuring until you realize the cap may not cover your actual loss. Compliance that keeps insurers financially sound is worth more than any safety net.

My practical advice: treat insurer compliance history the same way you treat a contractor’s license check. It takes five minutes on your state insurance department’s website to see whether an insurer has a pattern of enforcement actions. That five minutes is the most valuable due diligence you can do before signing a policy. For business owners managing cargo insurance for trucking operations, the stakes are even higher because a compliance failure at the carrier level can halt operations entirely.

Choose insurers that treat compliance as a competitive advantage, not a cost center. The difference shows up exactly when you need it most.

— Guyorguy

How Insuaria helps you start the insurance process the right way

Insuaria is built around the principle that an organized, well-documented insurance intake process is the foundation of compliance-aligned coverage. Whether you are a homeowner reviewing your property coverage or a business owner managing multiple lines of insurance, Insuaria’s intake forms help you organize the information licensed insurance professionals need to evaluate your coverage accurately.

Starting with a structured intake process means your licensed agency partner receives complete, organized information from the beginning. That reduces errors, speeds up the review process, and supports the kind of documentation that matters when claims arise. Insuaria does not provide insurance advice or bind coverage. All coverage decisions are made by licensed professionals who follow up after your intake submission.

Start your home insurance intake today, or if you are a business owner, explore the business insurance intake process designed for fleet operators and commercial clients.

FAQ

What is insurance compliance?

Insurance compliance is the set of legal and regulatory requirements that insurers, agents, and producers must follow to operate lawfully, maintain financial stability, and treat policyholders fairly. It covers solvency standards, claims handling timelines, licensing, fraud prevention, and consumer data protection.

Why do insurance regulations matter to homeowners?

Insurance regulations protect homeowners by requiring insurers to pay claims on defined timelines, maintain sufficient capital to cover losses, and handle policies without deceptive practices. States like Texas impose 18% annual penalty interest on insurers that miss prompt payment deadlines, giving homeowners direct legal recourse.

What happens if my insurer becomes insolvent?

State guaranty associations provide a financial backstop if your insurer becomes insolvent, but coverage caps typically range from $250,000 to $500,000 depending on the state and product. Claims exceeding those caps may not be fully recovered, which is why solvency compliance that prevents insurer collapse matters more than the safety net itself.

How can I check if my insurer has compliance violations?

Every state insurance department maintains a public record of enforcement actions, fines, and license suspensions. Searching your insurer’s name on your state department’s website takes minutes and reveals any pattern of market conduct violations or financial concerns.

What is a market conduct examination?

A market conduct examination is a formal regulatory review of how an insurer or agent treats policyholders, covering claims handling, underwriting, and sales practices. Failures identified in these exams lead to corrective action plans, fines, or license suspensions that directly affect the insurer’s ability to serve its customers.

Recommended

Comments