How to File Insurance Claims: A Step-by-Step Guide

- Guyorguy Laguerre

- 2 hours ago

- 9 min read

TL;DR:

Filing an insurance claim involves prompt notification and thorough documentation to ensure a smooth process. Proper preparation, including gathering photos, estimates, and reports, reduces delays and increases the likelihood of fair settlement. Effective communication with adjusters, respectful and factual, helps protect your interests and optimizes claim outcomes.

Filing an insurance claim is a formal request to your insurer asking for payment or coverage following a covered loss or event. Whether you’re dealing with storm damage to your home, a car accident, or a medical emergency, the file insurance claim process follows a predictable structure. Most people make costly mistakes not because they lack coverage, but because they don’t know what to submit, when to submit it, or how to communicate with their insurer. This guide walks you through every stage of the claims process, from gathering documentation to working with adjusters, so you can protect your payout and avoid unnecessary delays.

How to file insurance claims: what you need before you start

The single most important factor in a successful claim is preparation. Insurers require specific documentation to validate your loss, and missing even one item can stall your claim for weeks.

Core documents and information to collect

Before you contact your insurer, pull together the following:

Policy number and declarations page. Your declarations page summarizes your coverage limits, deductibles, and exclusions. Without it, you cannot confirm what your policy actually covers.

Incident details. Record the exact date, time, and location of the event. Write a factual description of what happened while your memory is fresh.

Photographic and video evidence. Photograph all damage from multiple angles before any cleanup or repairs begin. Courts and adjusters treat visual evidence as among the strongest proof of loss.

Receipts and repair estimates. Gather purchase receipts for damaged property and obtain at least one licensed contractor estimate for repairs.

Police or incident reports. For auto accidents, theft, or vandalism, a police report number is typically required. Request a copy directly from the responding agency.

Contact information for all parties. Collect names, phone numbers, and insurance details for any other drivers, witnesses, or contractors involved.

Maintaining a home inventory with photographs and receipts taken before any incident greatly simplifies claim validation and prevents disputes with adjusters.

Pro Tip: Create a dedicated digital folder immediately after an incident. Label subfolders by category: photos, estimates, correspondence, and policy documents. This single habit prevents the scramble that causes most claim delays.

Documentation deadlines you cannot miss

Timing matters more than most policyholders realize. Federal flood insurance requires submitting a signed proof of loss within 60 days, while many private insurers require the same form within 30 days. Missing these deadlines can result in a denied claim regardless of how valid your loss is. Check your policy’s specific requirements on the day of the incident, not the week before your deadline.

Document type | Why it matters |

Declarations page | Confirms coverage limits and deductibles |

Photographic evidence | Provides visual proof of damage before repairs |

Police or incident report | Required for theft, vandalism, and auto accidents |

Repair estimates | Establishes cost of loss for adjuster review |

Proof of loss form | Legally required within set deadlines for many policies |

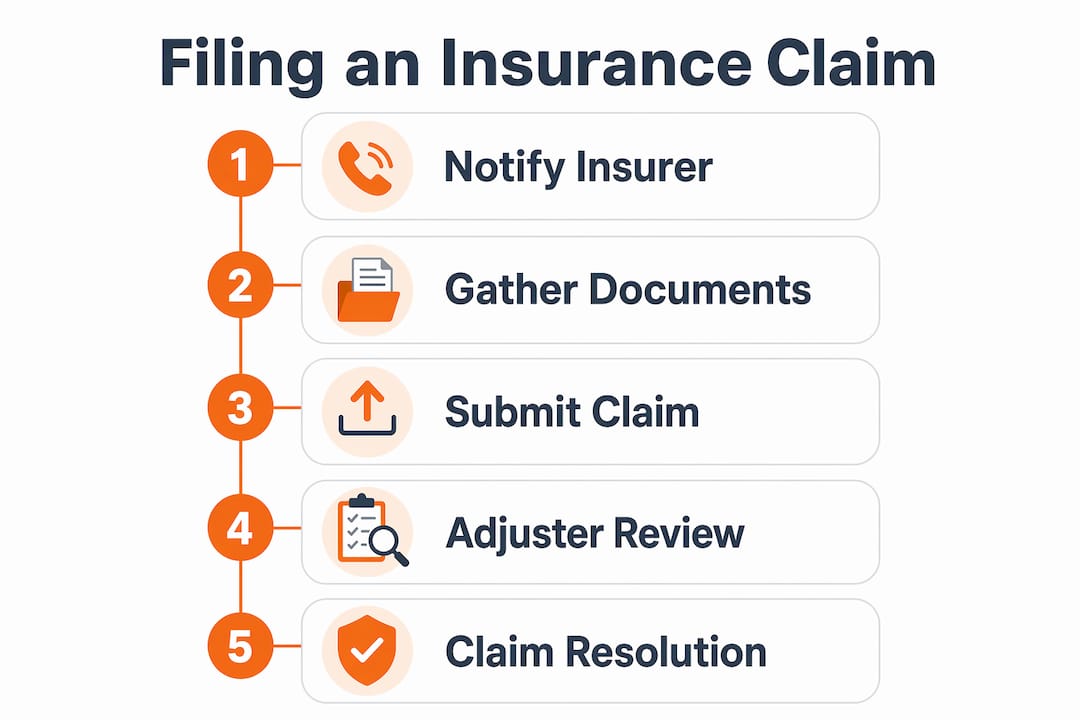

What are the steps to file a claim with your insurer?

The steps to file a claim follow a consistent sequence across home, auto, and health insurance. Knowing each stage in advance removes the guesswork and keeps your claim moving forward.

Notify your insurer immediately. Contact your insurance company by phone, mobile app, or online portal as soon as the incident occurs. Many policies require reporting an incident “as soon as reasonably possible,” and some auto policies set that window at 24 hours. Early reporting is directly correlated with faster, smoother claim resolution.

Complete the initial claim form accurately. Your insurer will provide a first notice of loss form. Fill in every field with factual information. Leave nothing blank. If a field does not apply to your situation, write “N/A” rather than skipping it.

Submit your documentation package. Upload or mail your photos, estimates, police reports, and receipts together. Submitting everything at once reduces back-and-forth with your insurer and shortens the review timeline.

Receive your claim number and adjuster assignment. Most U.S. states require insurers to acknowledge receipt of a claim within 10 to 15 days. That acknowledgment typically includes your claim number and the name of your assigned adjuster. Keep both on file.

Cooperate with the investigation. Your adjuster may schedule an on-site inspection, request additional documents, or ask follow-up questions. Respond to every request within the timeframe given. Delays on your end extend the overall timeline.

Review the settlement offer. Once the investigation closes, your insurer will issue a settlement offer. Compare it against your documented losses and your policy’s coverage limits before accepting.

Accept payment or dispute the offer. If the offer is fair, sign the release and receive payment. If it falls short, you have the right to negotiate. The dispute process is covered in the next section.

Pro Tip: After submitting documents, follow up in writing and ask your insurer to confirm receipt by email. This creates a paper trail that protects you if documents are later reported as missing.

Common submission methods include phone calls, insurer mobile apps such as those offered by State Farm or Allstate, and web portals. Apps and portals typically generate instant confirmation numbers, which is a meaningful advantage over phone-only reporting.

How do insurance adjusters work and what should you know?

An insurance adjuster is the insurer’s representative assigned to investigate your claim, assess the damage, and recommend a settlement amount. Understanding their role changes how you communicate and protects your interests throughout the process.

Adjusters work for the insurance company, not for you. Their job is to assess your claim accurately, but their employer’s financial interest is to settle claims at the lowest defensible amount. This is not a reason to be adversarial. It is a reason to be precise.

How to communicate effectively with your adjuster

Stick to documented facts in every conversation. Guessing or speculating about the cause of damage or the value of lost items harms your credibility. If you do not know an answer, say so directly. Adjusters are trained to identify inconsistencies, and a single contradictory statement can complicate an otherwise straightforward claim.

Key practices for adjuster communication:

Log every interaction. Note the date, time, name, and a summary of every conversation with your adjuster. Follow up with a brief email confirming what was discussed.

Provide your own estimates. You have the right to submit independent repair estimates from licensed contractors if the adjuster’s assessment seems low. Two or three competing estimates give you a factual basis for negotiation.

Do not accept verbal commitments. Ask for all decisions and offers in writing before acting on them.

Escalate when necessary. If you believe the adjuster’s assessment is inaccurate, request a supervisor review or file a formal complaint with your state’s department of insurance.

“Insurance agencies can provide valuable guidance, especially for complex claims, complementing direct insurer contact.” — Faculty Insurance

If a dispute cannot be resolved through internal escalation, most states allow policyholders to request appraisal or mediation. A public adjuster, who works exclusively for policyholders, is another option for large or contested claims.

What mistakes do people make when filing insurance claims?

The most common reason claims are delayed or denied is not fraud or lack of coverage. It is avoidable procedural errors made in the first 48 hours after an incident.

Errors that cost policyholders money

Delaying notification. Waiting days or weeks to report a loss gives insurers grounds to question the severity of damage and, in some cases, to deny the claim outright based on policy reporting requirements.

Incomplete documentation. Submitting photos without receipts, or estimates without a police report, forces adjusters to request additional materials. Each request adds days to your timeline.

Signing forms with blank fields. Never sign a claim form that contains empty sections. Cross out blank fields or write “N/A” to prevent unauthorized additions after your signature.

Failing to document insurer communications. Without written records of what was said and when, you have no recourse if your insurer later claims a document was never received or a commitment was never made.

Ignoring coverage limits and deductibles. Understanding your policy’s fine print, including exclusions and deductible thresholds, is the only way to make an informed decision about whether filing is financially worthwhile.

Pro Tip: Before filing a minor claim, calculate the cost of the loss against your deductible and the likely impact on your future premiums. For small losses, paying out of pocket often costs less over three to five years than the premium increase that follows a filed claim.

Filing versus paying out of pocket: a quick comparison

Scenario | File a claim | Pay out of pocket |

Loss significantly exceeds deductible | Recommended | Not practical |

Loss is close to or below deductible | Reconsider | Often better financially |

Third-party liability involved | Always file | Not an option |

First claim in several years | Lower premium risk | Consider either option |

Repeated claims in short period | High premium impact | Strongly consider self-pay |

For commercial vehicle operators, the calculus is similar but the stakes are higher. The truck insurance claims process involves additional regulatory requirements and documentation standards that differ from personal auto claims.

Key takeaways

Filing an insurance claim successfully requires prompt notification, complete documentation, and factual communication with your adjuster at every stage.

Point | Details |

Report immediately | Many policies require notice within 24 hours; early reporting speeds resolution. |

Build a document package | Gather photos, estimates, police reports, and your declarations page before contacting your insurer. |

Know your adjuster’s role | Adjusters represent the insurer; submit independent estimates if their assessment is low. |

Avoid blank form fields | Cross out or mark “N/A” on every empty section before signing any claim document. |

Calculate before filing | Compare your deductible and future premium impact against the loss amount before submitting minor claims. |

What I’ve learned from watching claims go right and wrong

Most people treat filing a claim as a reactive event. Something breaks, they call their insurer, and they hope for the best. The policyholders who consistently get fair settlements treat it as a process they manage, not one that happens to them.

The single biggest differentiator I’ve observed is documentation created before an incident. A homeowner who has a current photo inventory of every room, with serial numbers and purchase dates recorded, resolves claims in days. A homeowner who starts documenting after the loss spends weeks reconstructing what they owned and fighting for values the adjuster won’t accept without proof.

The second thing most guides won’t tell you is that patience is a strategy. Insurers process thousands of claims simultaneously. Adjusters who receive polite, organized, complete submissions move those files faster than the ones that require constant follow-up requests. Being the easiest file on an adjuster’s desk is not weakness. It is leverage.

I also think the “always file a claim” instinct is worth questioning. For a $1,200 fence repair with a $1,000 deductible, you are filing paperwork, inviting scrutiny of your property, and potentially triggering a premium review for a $200 net benefit. That math rarely works in your favor. Know your numbers before you pick up the phone.

Finally, the policyholders who struggle most are the ones who treat their insurer as an adversary from the first call. Adjusters are professionals doing a job. Factual, organized, respectful communication gets claims resolved. Hostility creates friction that slows everything down and rarely improves the outcome.

— Guyorguy

How Insuaria helps you organize your claim from the start

Filing a claim is only as smooth as the preparation behind it. Insuaria is a compliance-first intake and referral platform built to help homeowners, individuals, and business owners organize the information licensed insurance professionals need to review their coverage.

Through simple digital intake forms, Insuaria helps you pull together policy details, incident information, and supporting documents before a licensed agency partner follows up. Whether you need to organize a home insurance intake or share files securely with a professional, Insuaria gives you a structured starting point. Insuaria does not provide insurance advice or bind coverage. All coverage decisions are handled by licensed professionals. Start organizing your claim details at Insuaria today.

FAQ

What is the first step when filing an insurance claim?

Contact your insurer immediately after the incident by phone, app, or online portal. Many policies require notification within 24 hours, and early reporting is directly linked to faster claim resolution.

What documentation is required for an insurance claim?

Standard insurance claim documentation includes your policy number, a written incident description, photographs of the damage, repair estimates, and any police or incident reports. Missing documents are the most common cause of claim delays.

How long does it take for an insurer to process a claim?

Most U.S. states require insurers to acknowledge a claim within 10 to 15 days. Full processing timelines vary by claim type and complexity, but straightforward claims with complete documentation typically resolve faster.

Can I dispute a low settlement offer from my adjuster?

Yes. You have the right to submit independent repair estimates from licensed contractors if the adjuster’s figure seems low. You can also escalate to a supervisor, request mediation, or file a complaint with your state’s department of insurance.

Should I always file a claim for every loss?

Not always. For losses close to or below your deductible, calculating the financial impact on future premiums before filing is worth the time. Paying minor losses out of pocket often costs less over several years than the resulting premium increase.

Recommended

Comments