Cargo Insurance Workflow: A Guide for Logistics Managers

- Guyorguy Laguerre

- May 22

- 10 min read

TL;DR:

Getting cargo insurance wrong can turn a recoverable loss into a denied claim, causing significant financial and operational damage.

A well-structured workflow, including thorough documentation, timely notifications, and joint surveys, is essential for successful claim resolution.

Integrating insurance processes into transportation management systems enhances compliance and speeds up settlement times, reducing costs and risks.

Getting cargo insurance wrong costs businesses far more than the price of a lost shipment. A flawed cargo insurance workflow, specifically one with missed notifications, unsigned damage receipts, or fragmented documentation, turns a recoverable loss into a denied claim. The financial hit is obvious. The operational hit is worse: you’re left chasing carriers, disputing liability, and rebuilding customer trust simultaneously. This guide walks you through every phase of the cargo insurance process, from pre-shipment preparation through claim resolution, with enough specificity to actually change how your team operates.

Table of Contents

Key takeaways

Point | Details |

Document everything before loss | Organized invoices, bills of lading, and packing lists are your first line of defense when a claim is filed. |

Notify within 24 to 72 hours | Coverage rights erode fast after discovery; written notification to carriers and insurers must happen immediately. |

Never sign a clean receipt | Noting visible damage at delivery protects your claim; a clean signature can invalidate coverage entirely. |

Digital workflows cut claim time | Digitally documented claims can settle in under 14 days versus the standard 4 to 8 weeks. |

Errors before filing hurt most | The majority of denied claims trace back to preparation failures, not the coverage itself. |

Building your cargo insurance workflow foundation

Before any shipment leaves your dock, the groundwork for a successful claim should already be in place. Most logistics managers assume insurance is a reactive tool. The businesses with the best claim outcomes treat it as a pre-shipment discipline.

What documentation you actually need

The documents that support a cargo insurance claim fall into three categories: pre-shipment records, transit records, and delivery records. All three need to exist before a problem occurs, not after.

Pre-shipment records include the commercial invoice, packing list, letter of credit (if applicable), and the insurance certificate itself. Transit records include the bill of lading, air waybill, or sea waybill depending on mode. Delivery records are the ones most teams neglect: the signed delivery receipt with any damage notes, and photographs taken at the time of delivery.

Document | Stage | Responsible Party | Why It Matters |

Commercial invoice | Pre-shipment | Shipper | Establishes cargo value for claims |

Bill of lading | Transit | Carrier | Legal record of cargo condition at loading |

Packing list | Pre-shipment | Shipper | Confirms quantity and description |

Insurance certificate | Pre-shipment | Insured/Broker | Proves coverage was in force |

Delivery receipt with notes | Delivery | Consignee | Documents damage or shortage at receipt |

Survey report | Post-loss | Surveyor | Formal damage assessment for claim |

Understanding coverage types

Marine cargo insurance, which covers goods moving by sea, air, road, and rail, operates under three primary coverage tiers: Institute Cargo Clauses (ICC) A, B, and C. ICC A is the broadest, covering all risks of loss or damage except specific named exclusions. ICC B and C are narrower, covering only named perils. Most commercial shipments use ICC A, but the clause choice directly affects what you can claim and how. Cargo valuation for claims is typically based on invoice value plus freight cost, with an uplift of approximately 10% for anticipated profit. That means your coverage amount should reflect this formula, not just the raw invoice value.

Legal deadlines are the area where teams most frequently get burned. Under most policies, written notice of a claim must be submitted within three to seven days of delivery for visible damage, and within 14 to 30 days for concealed damage. Missing these windows gives insurers grounds to deny coverage regardless of the underlying merit.

Pro Tip: Link your insurance certificate and policy terms directly to each shipment record in your TMS or freight management platform. When a damage event occurs, your team will have the policy number, insurer contact, and coverage limits in the same place as the tracking data, cutting response time dramatically.

How to execute a cargo insurance claim, step by step

When damage or loss is discovered, most teams freeze or improvise. Neither response works. A well-rehearsed cargo insurance process eliminates both reactions and protects your claim from the start.

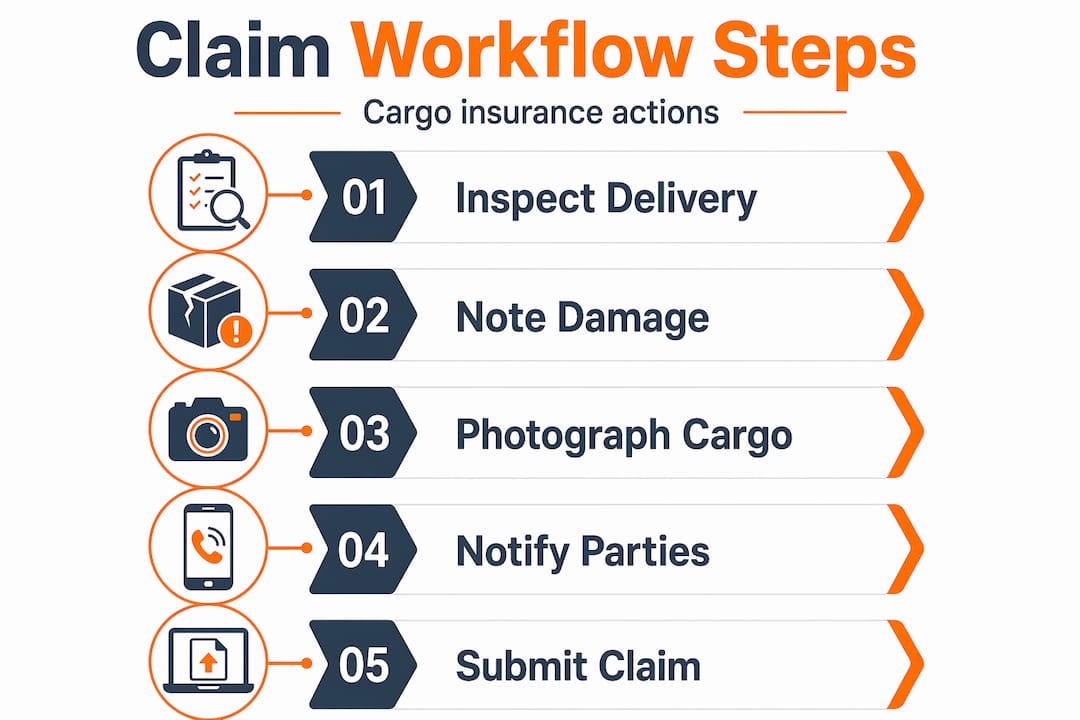

The nine steps of effective claim execution

Step 1: Inspect on delivery. Before the driver leaves, inspect the cargo. Look for visible damage, shortages, and signs of tampering. Do not let urgency override this step. If you cannot inspect fully, write “subject to inspection” on the delivery receipt.

Step 2: Note damage on the receipt. If you see damage, write it clearly on the delivery receipt before signing. Be specific: “two cartons crushed, moisture damage on southwest pallet.” A clean receipt without noted exceptions is one of the most common reasons cargo claims are denied.

Step 3: Photograph and video everything. Capture the cargo from multiple angles. Photograph the packaging, the labels, the damaged items, and the delivery vehicle if possible. Take photos before anything is moved or unpacked.

Step 4: Notify parties in writing within 24 to 72 hours. Cargo insurance notification should reach your carrier, freight forwarder, and insurer within this window. Use email so you have timestamps. Include a brief description of the damage, the shipment reference, and a statement that a formal claim will follow.

Step 5: Issue formal notice of loss to the carrier. This is separate from notifying your insurer. Failing to issue formal notice to carriers and bailees immediately often leads to insurers denying claims because the insurer loses its right of subrogation. Subrogation is the insurer’s right to pursue the responsible party for reimbursement after paying your claim. No notice means that right evaporates.

Step 6: Request a joint survey. Contact your insurer or their appointed surveyor and request a joint survey of the damaged goods. Not demanding a joint survey before moving or unpacking cargo is a fatal mistake that regularly causes claim denial due to lost evidence. The surveyor’s report becomes one of your most important claim documents.

Step 7: Hold the damaged goods. Do not dispose of, repair, or move the damaged cargo until the survey is complete. This seems obvious, but warehouse pressure often pushes teams to clear damaged goods quickly. Resist that pressure. Preserving evidence is a legal and contractual obligation under most policies.

Step 8: Compile your claim package. This is what experienced freight insurance managers call building a “paper fortress.” It includes every document from the table above, plus your notification emails, the survey report, the carrier’s response, and any repair or replacement invoices. The more complete the package, the faster and smoother the resolution.

Step 9: Submit the formal claim and follow up. Submit your claim package to the insurer in writing. Confirm receipt. Set a calendar reminder to follow up every seven to ten days until you receive a written acknowledgment and assigned claim number.

Pro Tip: Never unpack or sort damaged goods without at least photographing the sealed condition first. Insurers and surveyors need to assess damage in its discovered state. Even well-intentioned unpacking can destroy the evidentiary chain your claim depends on.

Common mistakes that kill cargo insurance claims

Understanding the cargo insurance workflow conceptually is one thing. Knowing exactly which errors destroy otherwise valid claims is what separates logistics teams that recover losses from those that absorb them.

The most costly mistakes rarely involve coverage gaps. They involve execution failures that occur in the first 72 hours after discovery.

Mistake | Why It Hurts Your Claim | Corrective Action |

Signing a clean delivery receipt | Waives right to claim visible damage | Always note exceptions before signing |

Late notification to insurer | Grounds for denial based on policy conditions | Notify within 24 to 72 hours, in writing |

No formal notice to carrier | Insurer loses subrogation rights | Send written notice same day as discovery |

Unpacking before survey | Destroys physical evidence chain | Hold cargo until surveyor confirms release |

Incomplete documentation | Delays claim, forces insurer to request more | Compile full document set before submitting |

Incorrect coverage amount | Claim paid at lower than actual loss | Calculate coverage using invoice plus freight plus 10% uplift |

Ignoring policy exclusions | Expecting coverage that never existed | Read policy before shipment, not after loss |

Beyond the table, there is a systemic issue that runs through all of these mistakes: fragmented documentation. Fragmented insurance documentation disconnected from shipment records causes claim delays and denials at a rate that surprises even experienced freight managers. When your insurance certificate lives in one system and your bill of lading lives in another, the gap between them becomes a liability.

The solution is integration. Embedding cargo insurance within your TMS eliminates data silos and improves compliance, audit trails, and claim resolution speed. It also means your team cannot forget to attach insurance documents to a shipment record because the system makes separation impossible.

You also need to watch for exclusions that are easy to overlook. Inherent vice (the natural tendency of some goods to deteriorate), inadequate packing, and delay damage are commonly excluded under all ICC clauses. If your goods are temperature sensitive, verify whether your policy specifically covers refrigeration failure. A standard cargo insurance policy often does not.

For a deeper breakdown of coverage scope and how it connects to your freight insurance management practices, see this guide to cargo coverage for trucking operations.

What happens after you file your claim

Filing the claim is not the finish line. It is the start of a process that can take days or months depending on how well your workflow held up before submission.

The standard claim lifecycle moves through four phases. First comes notification and acknowledgment, where your insurer confirms receipt and assigns an adjuster. Second is the assessment phase, where the adjuster reviews your documentation and may request the survey report or additional evidence. Third is the investigation phase, which applies to more complex claims and may involve independent surveyors, carrier interviews, or legal review. Fourth is settlement, where the insurer issues payment or a denial with reasons.

Standard cargo insurance claims typically take 4 to 8 weeks to resolve, but digitally documented claims can settle in under 14 days. Complex cases, such as total container losses or disputed liability, can run 6 to 12 months. The difference in outcome almost always traces back to documentation quality at the time of filing.

Digital and AI-enabled workflows are changing these timelines at the high end. AI-powered claims systems use computer vision and predictive analytics to resolve straightforward claims in hours instead of weeks. That is a meaningful operational advantage for businesses shipping at volume.

If your claim moves to dispute, you have several options:

Request a formal written explanation of any denial or underpayment

Engage an independent marine surveyor to contest the insurer’s damage assessment

Invoke the policy’s arbitration clause, which most marine cargo insurance policies include

Escalate to legal counsel if the disputed amount justifies it, typically above $25,000

Pro Tip: Keep a dedicated log for every claim in progress: dates of all communications, names of contacts, claim numbers, and deadlines. Insurers and adjusters handle hundreds of claims simultaneously. The logistics managers who get faster resolutions are invariably the ones following up with specifics, not general inquiries.

For a closer look at how this process applies to truck-based freight, Insuaria’s guide on how to handle truck insurance claims covers the carrier-side dynamics in practical detail.

My honest take on where cargo workflows break down

I’ve watched businesses lose six-figure claims not because they lacked coverage, but because their team did not know what to do in the first three hours after discovering damage. Coverage without workflow discipline is expensive window dressing.

The hardest truth I’ve come to accept is that most cargo claim denials are self-inflicted. A clean signature on a damaged receipt. A call to the insurer on day four instead of day one. Photographs taken after a forklift operator already moved the pallet. Each of these sounds like a small misstep, but to an insurer reviewing subrogation rights, they read as procedural failures that justify denial.

What I’ve seen work, consistently, is treating the insurance claims workflow the same way you treat a safety protocol. You do not improvise safety procedures on the floor. You train people, post checklists, and run drills. The same discipline needs to apply to cargo damage response. Your warehouse team, your drivers, and your logistics coordinators all need a laminated card or a phone-accessible checklist that tells them exactly what to do in the first 72 hours.

The technology shift is real and accelerating. Digital end-to-end claims workflows already reduce processing times by 50%, and the businesses investing in this now will have a material cost and compliance advantage in three years. But technology does not fix a culture that deprioritizes documentation. The tool only works if the habit exists.

Build internal champions. Pick one person per location, or one per major trade lane, who owns the cargo insurance process. Not HR. Not accounting. Someone in operations who understands that their job performance connects directly to claim outcomes.

— Guyorguy

How Insuaria helps you get your cargo insurance process right

Getting your cargo insurance workflow organized before a loss event is the difference between a fast settlement and a prolonged dispute. Insuaria was built for exactly this situation. The platform gives business owners and logistics managers a structured way to organize their insurance information and submit it to licensed insurance professionals who can review actual coverage needs.

Through simple intake forms, Insuaria helps you pull together the details that matter most before a licensed agency partner reviews your situation. Whether you are managing trucking fleets, coordinating international freight, or building a more structured transportation insurance process across your business, starting with organized intake is the step most businesses skip.

Review Insuaria’s terms and conditions to understand how the platform operates, and start your organized insurance intake process through Insuaria’s business intake page. Insuaria does not bind coverage or issue quotes. All coverage decisions are made solely by licensed insurance professionals following your submission.

FAQ

What is a cargo insurance workflow?

A cargo insurance workflow is the structured sequence of steps a business follows to prepare for, document, report, and resolve cargo insurance claims. It covers pre-shipment documentation, damage notification, evidence collection, claim submission, and follow-up through settlement.

How soon must you notify your insurer after cargo damage?

Notification best practice is within 24 to 72 hours of discovery. Some policies allow up to 30 days, but delays increase the risk of denial, especially for time-sensitive evidence requirements like joint surveys.

What documents do you need to file a cargo insurance claim?

You need the commercial invoice, bill of lading, packing list, insurance certificate, delivery receipt noting the damage, photographic evidence, and a survey report. Missing any of these can delay or reduce your settlement.

Why do cargo insurance claims get denied?

Most denials trace back to procedural failures: signing a clean delivery receipt, late notification, failure to request a joint survey, or insufficient documentation. The coverage itself is rarely the issue when claims are denied.

How long does a cargo insurance claim take to resolve?

Standard claims resolve in 4 to 8 weeks. Digitally documented claims with complete evidence packages can settle in under 14 days. Complex or disputed claims may take 6 to 12 months depending on investigation requirements.

Recommended

Comments