The Role of Compliance in Trucking Insurance

- Guyorguy Laguerre

- May 21

- 10 min read

TL;DR:

Many fleet operators mistakenly see insurance and compliance as separate issues, risking suspension or doubled premiums.

Maintaining active, accurate FMCSA filings, including BMC-91 and MCS-90, is essential for legal operation and cost control.

Most fleet operators think about insurance and compliance as two separate problems. One sits in your filing cabinet, the other in your broker’s inbox. That separation is exactly what gets carriers into trouble. The role of compliance in trucking insurance is not a background detail. It determines whether your policy is valid, what you pay in premiums, and whether you can legally move freight at all. Get it wrong and you are not just facing a fine. You are looking at suspended operating authority, denied claims, and insurance premiums that can double overnight.

Table of Contents

Key Takeaways

Point | Details |

Compliance shapes insurance costs | CSA scores, loss history, and filing accuracy directly influence what underwriters charge your fleet. |

Filing errors trigger suspensions | Mismatched names or delayed BMC-91 filings can revoke operating authority within 30 days. |

Federal minimums are dangerously low | The $750,000 minimum covers less than 2% of modern catastrophic injury verdicts. |

Continuous coverage is non-negotiable | Even a 24-hour gap in recognized coverage can trigger revocation that costs thousands to reinstate. |

Compliance is a cost-saving system | Operators who treat compliance as an ongoing system reduce premiums and negotiate stronger policy terms. |

The role of compliance in trucking insurance starts here

Before a single truck moves freight under your authority, the Federal Motor Carrier Safety Administration (FMCSA) requires documented proof of financial responsibility. This is not optional paperwork. It is the legal mechanism that activates your operating authority and defines the minimum insurance thresholds your policy must meet.

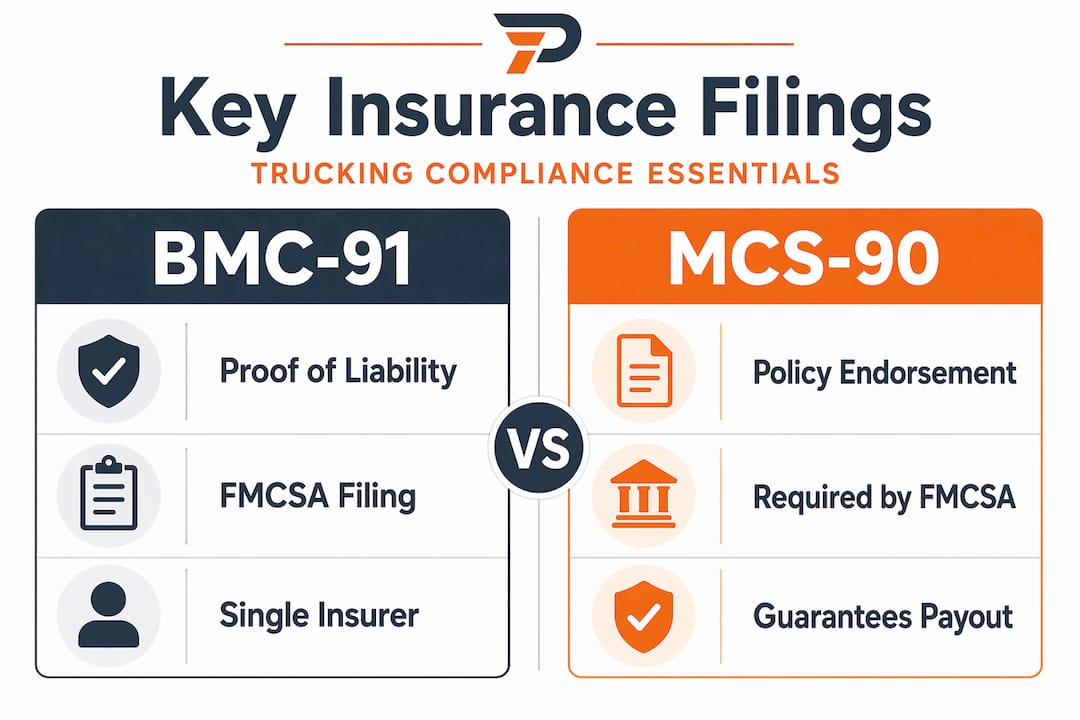

The two filings that matter most are the BMC-91 and the MCS-90 endorsement. The BMC-91 is the electronic insurance filing your insurer submits directly to FMCSA on your behalf, confirming that your policy meets federal minimums. The MCS-90 endorsement is attached to your policy and guarantees public compensation even when the underlying policy might otherwise exclude a claim. Together, they are the legal backbone of your operating authority.

Federal minimum thresholds vary by cargo type. For-hire carriers hauling non-hazardous freight in vehicles over 10,001 pounds must carry at least $750,000 in public liability coverage. Carriers transporting hazardous materials face minimums up to $5,000,000. These numbers represent a legal floor, not an adequate ceiling. More on that distinction shortly.

Here is where regulatory compliance for trucking connects directly to your insurance eligibility: your policy must remain active and properly filed at all times. FMCSA verifies this through the publicly accessible Licensing and Insurance (L&I) portal. Brokers, shippers, and auditors check this portal routinely. If your filing status shows anything other than “active,” freight contracts disappear fast.

Your insurer must file the BMC-91 before your operating authority activates.

The MCS-90 must be attached to every primary liability policy covering interstate operations.

Coverage must remain continuous. Any lapse triggers an automatic suspension process.

FMCSA auditors cross-reference your carrier profile, fleet size, and safety data against your insurance records.

Both your legal business name and your FMCSA-registered name must match your insurer’s filings exactly.

Pro Tip: Pull up your FMCSA L&I portal listing right now and verify your filing status. Many operators discover stale or misfiled records only when a broker flags them before a load, which is the worst possible time to find out.

How compliance performance drives your premium costs

Underwriters do not price trucking policies on gut feeling. They use data, and most of that data comes from your compliance record. Understanding this connection is how serious fleet operators stop overpaying and start using compliance as a financial tool.

New authority carriers feel this reality immediately. New carriers typically pay 50 to 100% more in their first year, with annual primary liability premiums ranging from $8,000 to $18,000. The reason is straightforward: no safety history means no evidence of low risk. As you build a clean loss record, those premiums can drop by 30 to 40% in subsequent years.

The data points underwriters examine most closely include:

CSA scores. The Compliance, Safety, Accountability system measures seven Behavior Analysis and Safety Improvement Categories (BASICs). High scores in categories like Hours of Service Compliance or Unsafe Driving signal elevated risk to underwriters and typically push premiums upward.

Driver Motor Vehicle Records (MVRs). A single driver with multiple violations can increase your fleet’s overall risk profile. Underwriters review MVRs for every driver on your policy, and patterns of violations translate directly into higher rates.

Loss history. Claims frequency and severity over the prior three to five years are among the strongest predictors underwriters use. A fleet with zero at-fault losses and a clean CSA profile gets treated very differently than one with two liability claims and open FMCSA investigations.

Safety program documentation. Carriers with documented drug and alcohol testing programs, structured driver orientation, and regular vehicle inspection logs signal to insurers that risk is managed proactively.

Insurance carriers increasingly use FMCSA safety and loss data as leading indicators when adjusting premium offers, which means your compliance record is effectively a pricing document. Every roadside inspection outcome, every violation, every open investigation is visible and being used against or in favor of your renewal rate.

The importance of compliance in trucking extends beyond avoiding fines. A clean compliance profile is the single most controllable variable in what you pay for coverage. Improving your CSA scores and reducing your premium costs is not a passive process. It requires deliberate, system-level attention to how your fleet operates every day.

Compliance pitfalls that kill coverage and authority

You can be paying your premiums on time every month and still lose your operating authority. The mechanism is almost always a filing error or a lapse in the insurance record. Understanding exactly how these failures happen is the difference between staying on the road and sitting idle.

The most dangerous pitfall is an insurance lapse. If your insurer cancels your policy or your coverage lapses, they are required to notify FMCSA. An automatic authority suspension follows within 30 to 35 days if a new BMC-91 is not submitted to replace the cancelled filing. That window sounds generous until you factor in weekends, holidays, and insurer processing time. Reinstatement after a suspension requires reapplication, fees, and potential re-review. The operational downtime alone can cost a mid-size fleet tens of thousands of dollars.

Filing accuracy is the second major risk area. FMCSA’s electronic system matches your insurer’s submission against your registered carrier profile. Minor name discrepancies on BMC-91 filings cause automatic rejection and trigger suspension notices. If your legal business name changed due to an acquisition, restructuring, or simple clerical update, every insurance filing must reflect that exact current name. One word off is enough for the system to reject the submission.

Outdated MCS-150 filings. Your MCS-150 biennial update must reflect your current fleet size and operations. Mismatches between your MCS-150 data and your insurance policy coverage amounts create audit red flags.

Umbrella policy transitions. When you add an umbrella or excess policy, you must switch from BMC-91 to BMC-91X filing to cover multi-insurer arrangements. Failing to update this filing triggers immediate suspension notices, even if your underlying coverage is fully paid and active.

Driver-vehicle record mismatches. If your policy lists 12 power units but your MCS-150 reports 18, that discrepancy invites a compliance review.

Stale agent relationships. Operators who switch insurance agencies mid-term sometimes discover the outgoing agency failed to properly cancel the old filing before the new one was submitted, creating overlapping or conflicting records.

Pro Tip: Every time your policy renews, changes carriers, or adds a layer of coverage, treat the FMCSA filing update as the final step before you consider the transaction complete. Do not assume your broker or agent handled it automatically.

Beyond minimums: closing the liability gap

The $750,000 federal minimum has not been substantially updated in decades. The trucking industry has changed dramatically. Litigation verdicts have not. The gap between what the law requires and what a catastrophic accident actually costs is staggering, and it is getting wider every year.

Modern catastrophic injury verdicts average approximately $51 million. The federal minimum covers less than 2% of that exposure. Technically, you are compliant at $750,000. Practically, a single serious accident can bankrupt your company despite having insurance. This is why the importance of compliance in trucking cannot be separated from intelligent coverage strategy.

The comparison below shows the real exposure gap fleet operators face:

Coverage level | What it covers | What it leaves exposed |

$750K federal minimum | Basic public liability, legally required | 98%+ of catastrophic verdict exposure |

$1M primary liability | Meets most broker requirements | Multi-vehicle accidents, severe injury claims |

$1M + $4M umbrella | Significant verdict protection | Major multi-claimant events, nuclear verdicts |

$1M + $9M umbrella | Strong protection for mid-size fleets | Rare but real catastrophic multi-fatality events |

Most freight brokers today require primary liability of at least $1 million as a contractual condition for carrier onboarding. Many require umbrella coverage on top. If your trucking liability coverage does not meet broker minimums, you simply do not get the load. That is a revenue problem, not just a risk management problem.

Adding umbrella coverage also means changing your FMCSA filings. Moving from a single-insurer arrangement to a layered policy requires a BMC-91X filing in place of the standard BMC-91. Missing this step means your umbrella policy exists on paper but is not recognized by FMCSA, leaving you exposed to suspension and unprotected in the event of a claim that pierces your primary limit.

Operators who build their compliance systems to handle layered coverage from the start find that insurers respond with better renewal terms. Compliance as an integrated system is what separates operators who negotiate from a position of strength versus those who take whatever renewal rate their broker presents.

Best practices to protect your coverage and lower costs

Trucking risk management at the fleet level is not about responding to problems. It is about building processes that prevent them. The operators with the best insurance outcomes all share one characteristic: they treat compliance as a year-round operational function, not an annual checkbox.

Here are the practices that separate compliant, cost-efficient fleets from those constantly putting out fires:

Centralize your compliance documentation. Use a single system, whether a transportation management system (TMS) or a dedicated compliance platform, to store driver files, vehicle inspection records, training logs, and insurance documents. Integrated ELD and safety data systems reduce audit failures and prevent the gaps that drive premium increases.

Monitor your FMCSA L&I portal regularly. Set a weekly calendar reminder to check your carrier profile. Even 24-hour gaps in recognized coverage risk revocation. Do not rely solely on your insurer to alert you to a lapse. Verify it yourself.

Automate premium payments. A missed payment due to cash flow timing or a banking error is one of the most common causes of policy cancellation and subsequent FMCSA notification. Autopay with a backup funding source eliminates this risk entirely.

Communicate fleet changes to your agent proactively. Every time you add a vehicle, remove a driver, or change your operating radius, your policy details and FMCSA filings may need updating. Waiting until renewal creates gaps that underwriters notice.

Invest in a formal safety program. Driver scorecards, structured onboarding, regular MVR reviews, and documented pre-trip inspections improve CSA scores over time. Better CSA scores mean better renewal pricing and stronger standing when negotiating insurance terms for your fleet.

Pro Tip: Ask your insurance agent to send you a copy of every FMCSA filing they submit on your behalf. Build a folder of these confirmations. During an audit, having immediate access to your full filing history demonstrates the kind of operational maturity that auditors and underwriters both reward.

My honest take on what separates surviving fleets from struggling ones

I have spent years watching fleet operators approach compliance the same wrong way: treat it as a legal burden, hand it off to someone else, and hope nothing bad happens. The operators who exit the market early almost always follow that exact pattern.

Here is what I have actually seen work. Compliance is not a department. It is a mindset that has to live in your daily operations. The carriers who survive long-term treat every driver MVR pull, every inspection result, and every FMCSA filing as a direct investment in their insurance standing. Because that is exactly what it is.

The mistake I see most often is operators who pay their premiums on time but ignore everything else. They think coverage equals protection. What they do not realize is that a lapse in filing, a name mismatch, or a single missed umbrella update can void the protection they thought they were paying for. Compliance failures compound, and tens of thousands of carriers exit the market every year because of risk failures that accumulated quietly while owners focused on loads and revenue.

The other thing most articles will not tell you: your compliance record is a negotiating tool. Walk into a renewal conversation with clean CSA scores, no claims in 36 months, and documented safety systems and your broker suddenly has something to work with. Underwriters compete for that kind of account. That competition shows up in your premium. Ignore compliance and you take whatever rate you are given, usually because there are not many markets willing to write you at all.

The trucking operators I respect most do not ask “what do I have to do to stay legal?” They ask “what does my compliance record say about how I run this business?” That shift in framing changes every decision that follows.

— Guyorguy

How Insuaria helps fleet operators stay ahead

Managing BMC-91 filings, MCS-90 endorsements, and layered coverage arrangements takes time and precision. One error resets your operating authority and costs you freight contracts you cannot afford to lose. Insuaria is built to make the first step of that process faster and less stressful for fleet operators who are already stretched thin.

Through Insuaria’s business insurance intake platform, you can organize the compliance and coverage details that licensed insurance professionals need to review your trucking coverage. Rather than hunting down documents during a renewal conversation, you submit your fleet information through a structured intake form. From there, a licensed agency partner follows up to handle the actual coverage decisions, filings, and recommendations.

Insuaria is not an insurance company or carrier, but it is a compliance-aware platform that understands what trucking businesses need to bring to the insurance conversation. Whether you are managing a single authority or coordinating coverage across a growing fleet, getting your information organized is the first step toward better outcomes. Start that process now before your next renewal catches you scrambling.

FAQ

What is the role of compliance in trucking insurance?

Compliance directly determines your insurance eligibility, premium pricing, and whether your policy is legally recognized by FMCSA. A clean compliance record lowers costs and keeps your operating authority active.

How do filing errors affect trucking operating authority?

A name mismatch or missed BMC-91 filing can trigger automatic suspension of your operating authority within 30 to 35 days. Reinstatement requires fees and processing time that costs fleets significant revenue.

Why is the $750,000 federal minimum not enough coverage?

The federal minimum covers less than 2% of the average catastrophic injury verdict, which runs around $51 million. Most freight brokers also require at least $1 million in primary liability as a contract condition.

What is the difference between BMC-91 and BMC-91X?

BMC-91 covers single-insurer arrangements, while BMC-91X is required when you carry layered coverage across multiple insurers, such as a primary policy plus an umbrella. Using the wrong filing type triggers suspension.

How can fleet operators lower their trucking insurance premiums through compliance?

Improving CSA scores, maintaining a clean loss history, and documenting formal safety programs are the most direct ways to reduce premiums. Carriers with clean records can see 30 to 40% decreases compared to their first-year rates.

Recommended

Comments