The Role of Insurance Certificates in Trucking Compliance

- Guyorguy Laguerre

- May 23

- 11 min read

TL;DR:

Many trucking operators misunderstand that certificates of insurance are only informational and do not grant coverage or extend policy limits.

Maintaining active FMCSA filings via insurer submissions is essential, as even a 24-hour lapse triggers automatic authority revocation without notice.

Properly distinguishing between certificate holders and additional insureds is critical for legal protection; only endorsements confer actual liability coverage under your policy.

Insurance certificates are one of the most misread documents in trucking. Fleet operators collect them, shippers demand them, and brokers require them before giving a load. Yet a surprising number of carriers treat them as a formality rather than a functional compliance tool. Understanding the real role of insurance certificates in trucking means knowing not just what they show, but what they do and do not protect. This guide breaks down the regulatory mechanics, common misconceptions, and practical strategies that separate compliant fleets from those that lose their operating authority without warning.

Table of Contents

Key takeaways

Point | Details |

COIs prove coverage, not grant it | A certificate of insurance is informational only and does not change or extend policy coverage. |

FMCSA filings override COI possession | Active BMC-91 or BMC-91X electronic filings by your insurer determine operating authority, not holding a COI. |

Certificate holder does not equal insured | Being listed as a certificate holder provides no coverage rights. Only an additional insured endorsement does. |

A one-day filing gap costs authority | FMCSA systems trigger automatic revocation with no grace period for even a 24-hour lapse in insurer filings. |

Broker minimums often exceed legal limits | Many brokers require $1,000,000 in liability even when FMCSA requires $750,000 for the same freight type. |

The role of insurance certificates in trucking operations

A Certificate of Insurance, or COI, is a one-page document issued by your insurer or broker that summarizes your active coverage. It lists the insurer name, policy number, coverage types, limits, effective dates, and the named insured. In trucking, COIs travel constantly between carriers, shippers, freight brokers, and ports. They are the standard answer to “prove you’re insured.”

But here is where most operators make their first mistake. A COI is informational only and does not provide coverage or amend the policy in any way. It is a snapshot, not a contract. The actual coverage lives in the policy document itself, and any rights, exclusions, or endorsements are governed by that policy, not by what appears on the certificate.

In trucking, the role of certificates of insurance extends into several practical areas:

Confirming to shippers and freight brokers that your operation is currently insured before they assign loads

Satisfying contract requirements that specify minimum coverage types and limits

Supporting FMCSA licensing reviews and onboarding processes with new commercial partners

Demonstrating proof of financial responsibility during audits or after accidents

Providing a quick reference for policy details without pulling the full policy document

The COI does not grant trust by itself. It reflects the trust you have already built through properly maintained coverage and accurate filings. Shippers rely on COIs to vet carriers before a relationship starts, but that protection stops the moment the document is treated as a substitute for ongoing compliance.

One nuance worth understanding: the named insured on your COI must match the legal entity registered with the FMCSA exactly. A mismatch between your operating authority name and your COI can cause confusion during claims, contract review, or federal audits. Even a small variation, like “LLC” versus “Inc.”, can trigger disputes that delay payments or create coverage gaps.

FMCSA filing requirements and insurance certificates

Holding a COI is not enough to maintain your operating authority. The FMCSA requires motor carriers to keep active proof of financial responsibility on file electronically, and that filing must come directly from your insurer, not from you.

The two primary filing forms are BMC-91 and BMC-91X. The BMC-91 covers primary liability policies, while the BMC-91X handles excess or umbrella coverage layers. Both must be submitted by the insurer to FMCSA when a policy is issued and kept current throughout the policy term. Minimum liability limits range from $300,000 for smaller non-hazardous freight to $5,000,000 for certain hazardous materials, depending on cargo type and vehicle weight.

Here is the process that responsible fleet operators follow to stay ahead of filing risks:

Confirm with your insurer or broker the exact date they will submit BMC-91 or BMC-91X filings to FMCSA before your new policy takes effect.

Log into the FMCSA Licensing and Insurance Portal (L&I Portal) within 48 hours of your policy effective date to verify the filing appears correctly and matches your operating authority name.

Check that your named insured, policy limits, and effective dates on file with FMCSA exactly match the COI your broker issued.

Set a calendar reminder 60 days before renewal to prompt your insurer to submit updated filings before the current policy expires.

If your coverage uses layered or excess policies, confirm your agent filed the BMC-91X, not just the BMC-91. Many carriers face authority suspensions because agents file only the primary policy and overlook the excess layer.

The MCS-90 endorsement adds another layer of complexity. It is a federal endorsement attached to your liability policy that guarantees payment of third-party claims regardless of whether your policy would otherwise exclude the claim. That sounds like a safety net. It is not. The MCS-90 carries a Right of Reimbursement clause, meaning your insurer can pay the claim and then come back to you for repayment if the loss fell outside your actual policy terms. Treating the MCS-90 as a coverage backstop while skimping on proper liability coverage is one of the most expensive mistakes a carrier can make.

FMCSA’s automated system does not differentiate between a temporary filing lapse and a permanent cancellation. A single day without an active electronic filing triggers a notice of intent to revoke your operating authority. There is no grace period.

Pro Tip: Set a reminder to verify your FMCSA filing status at least 60 days before renewal, not 30. Insurers occasionally need lead time to process endorsements and submit filings, and a last-minute scramble is how one-day gaps happen.

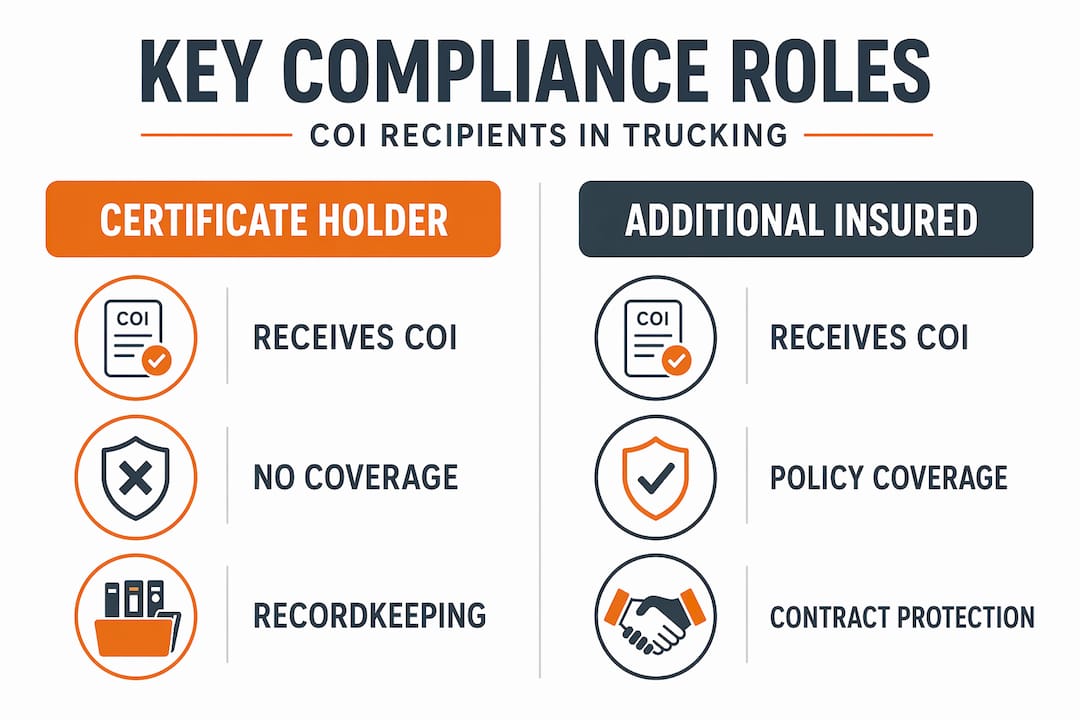

Certificate holders vs. additional insureds in trucking

This is the distinction that causes more disputes, denied claims, and contract conflicts than almost anything else in trucking insurance. And yet, the majority of fleet operators still get it wrong.

A certificate holder is simply the party that receives a copy of the COI for their records. Being listed as a certificate holder does not give that party any coverage rights whatsoever. They receive the document. That is the full extent of what the designation means.

An additional insured is an entirely different classification. When a party is added as an additional insured by formal policy endorsement, they receive actual liability protection under your policy for claims that arise from your operations. This is a legal modification of your policy, not just a paperwork formality.

Here is a side-by-side comparison to make this concrete:

Feature | Certificate Holder | Additional Insured |

Receives copy of COI | Yes | Yes (typically) |

Coverage rights under the policy | No | Yes, within endorsement scope |

Can file a claim directly | No | Yes |

Requires formal policy endorsement | No | Yes |

Common in trucking contracts | As default | Required by many brokers and shippers |

Listing a broker or shipper as a certificate holder on your COI does not provide them any insurance protection. If they want coverage for claims tied to your operations, they need to be named as an additional insured through a formal endorsement to your policy.

This matters enormously in contract situations. A freight broker may send you a contract that says “carrier must name broker as additional insured.” If you simply list them as a certificate holder and move on, that contract term is unfulfilled. If a claim arises, the broker will find they have no coverage under your policy, and you may be in breach of contract.

Certificate holders do not receive insurance coverage by default, and only an additional insured endorsement modifies the policy to extend coverage rights. Verifying that distinction before signing any broker agreement protects both your operations and your business relationships.

Pro Tip: When a contract requires additional insured status, ask your insurer to send you the actual endorsement page, not just a revised COI. The endorsement is the legal document. The COI is just the summary.

Best practices for managing trucking insurance certificates

Compliance is not a one-time event. It is a system. Fleet operators who stay out of trouble treat insurance certificate management as an ongoing process, not a box they checked at policy inception.

Here are the practices that separate operationally stable fleets from those that face surprise authority revocations:

Keep your FMCSA filing status verified on a monthly basis. Log into the L&I Portal and confirm your BMC-91 or BMC-91X shows as active. Insurers occasionally make administrative errors that affect filings without notifying the carrier.

Match all names precisely. Your legal operating entity name on your COI, your FMCSA operating authority, and your policy documents must be identical. Differences create gaps that are difficult to resolve quickly under pressure.

Request and store all endorsement pages. Do not accept a revised COI as proof that an endorsement exists. Ask for the actual endorsement document and keep it with your compliance files.

Coordinate renewals with your broker early. A single day of lapse in your insurer’s electronic filing triggers automatic authority revocation. Starting renewal coordination 60 days out gives you adequate runway.

Audit your additional insured endorsements quarterly. Broker agreements change, contracts are added, and endorsements that were active last year may not match your current contractual obligations.

Verify correct coverage levels meet broker requirements. Carrier contracts frequently specify limits that exceed FMCSA minimums, so confirming your COI reflects the right numbers before presenting it can prevent rejected loads or contract disputes.

A common operational mistake is delegating certificate tracking entirely to a broker without building any internal verification step. Brokers serve multiple clients and cannot always catch every filing issue specific to your authority. Keeping at least one internal point of contact who monitors the FMCSA insurance requirements for your operating authority adds a layer of protection that no outsourced relationship can fully replace.

Pro Tip: Create a compliance calendar that treats your FMCSA filing verification as a recurring monthly task, not something you only check at renewal. Fifteen minutes once a month can prevent a revocation that shuts you down for days.

Liability coverage types shown on insurance certificates

The numbers on your COI are not just for show. They tell shippers, brokers, and regulators exactly what financial protection you carry, and those numbers need to be right.

The core liability coverage in trucking is Bodily Injury and Property Damage, commonly called BIPD. This is the coverage that protects the public if your truck causes an accident. FMCSA sets minimum BIPD limits based on freight type and vehicle weight, and those minimums are not suggestions. Operating below them puts your authority at risk.

Here is a reference table for common FMCSA minimum liability limits:

Carrier Type | Cargo/Operation | FMCSA Minimum BIPD Limit |

For-hire carriers (non-hazmat) | General freight under 10,001 lbs | $300,000 |

For-hire carriers (non-hazmat) | General freight 10,001+ lbs | $750,000 |

For-hire carriers (hazmat) | Certain hazardous materials | $1,000,000 |

For-hire carriers (hazmat) | Highest risk hazmat categories | $5,000,000 |

Beyond BIPD, your COI may also reference cargo insurance, physical damage coverage, trailer interchange, and general liability. Each of these covers a different exposure, and many freight brokers require all of them before onboarding a carrier. Broker onboarding often demands $1,000,000 in liability even when FMCSA technically requires only $750,000 for the same freight, so your COI needs to reflect the higher number if that is what the contract specifies.

Incorrect or incomplete coverage types shown on your COI create real problems. If your COI shows cargo coverage but your actual policy has a bulk commodity exclusion that applies to the freight you’re hauling, you have a documentation gap that could deny a claim. The goal is alignment: your policy, your COI, and the contractual requirements you have agreed to should all say the same thing. You can review liability coverage types for trucking fleets to make sure your current COI reflects all required coverage categories accurately before presenting it to a new partner.

My take on what most fleets get wrong

I’ve reviewed enough trucking compliance situations to tell you plainly: the most dangerous place for a fleet operator is confident ignorance about insurance certificates. Not total ignorance. Confident ignorance. The operators who know just enough to feel like their paperwork is in order, but have never actually verified the details.

In my experience, the single most common reason carriers lose authority is not a refusal to pay premiums. It is a filing coordination failure between the carrier, their agent, and FMCSA. The insurer changes a billing system, the agent submits the BMC-91 two days late, and the carrier has no idea until loads start getting rejected because their authority shows as revoked. I’ve seen this happen to fleets running 20 trucks with otherwise solid operations.

The MCS-90 endorsement misunderstanding is the second issue that concerns me. Too many operators hear that the MCS-90 “guarantees” third-party claim payment and conclude that their underlying coverage does not need to be tight. That logic is backward. The Right of Reimbursement clause means your insurer can pursue you personally to recover what they paid on a claim your policy should have covered. The MCS-90 protects the public, not you.

What I recommend is a quarterly compliance review that covers three things: verification of active FMCSA filings in the L&I Portal, confirmation that all required endorsements (additional insured, MCS-90, BMC-91X if applicable) match current contracts and operating conditions, and a side-by-side comparison of your COI limits against every active broker agreement you have. That review takes less than two hours and has kept many fleets from learning these lessons the expensive way.

Proper insurance certificate management is not about being bureaucratically thorough. It is about protecting the revenue your operation depends on, every single day.

— Guyorguy

How Insuaria helps fleet operators stay organized

Managing insurance certificates, FMCSA filings, and endorsements across a growing fleet is a lot to track. Insuaria is built for exactly that kind of organizational challenge.

Insuaria is a compliance-first insurance intake and referral platform that helps trucking businesses and fleet operators organize the information licensed insurance professionals need to review their coverage. Through structured intake forms and educational tools, Insuaria makes it easier to submit your fleet details, document your coverage needs, and connect with the right professionals efficiently. If your current process relies on scattered emails and COIs saved in random folders, the trucking insurance intake process at Insuaria gives you a cleaner starting point. For fleet operators who want a more organized approach to their overall business insurance picture, the business insurance intake page walks you through a structured submission process designed specifically for operations like yours.

Insuaria does not bind coverage or issue quotes. Licensed insurance professionals follow up to handle all coverage decisions.

FAQ

What is a certificate of insurance in trucking?

A certificate of insurance is a one-page document that summarizes your active policy details, including coverage types, limits, insurer name, and effective dates. It serves as proof of insurance but does not grant or extend coverage on its own.

Does holding a COI satisfy FMCSA insurance requirements?

No. FMCSA requires active electronic filings submitted directly by your insurer via BMC-91 or BMC-91X forms. Possessing a COI does not fulfill this obligation or protect your operating authority from revocation.

What is the difference between a certificate holder and an additional insured?

A certificate holder simply receives a copy of the COI for recordkeeping. An additional insured is added to the policy through a formal endorsement and receives actual liability coverage under that policy. The two are not interchangeable.

How quickly can a filing lapse affect my operating authority?

A 24-hour gap in your insurer’s electronic filing to FMCSA is enough to trigger an automatic notice of intent to revoke your operating authority. There is no grace period in FMCSA’s automated system.

Why do brokers require higher insurance limits than FMCSA minimums?

Freight brokers often require $1,000,000 in liability coverage even when FMCSA requires $750,000 for the same freight type, because they manage their own risk exposure through carrier contracts. Your COI must reflect the limits specified in each broker agreement you operate under.

Recommended

Comments