Motor carrier insurance: complete guide for fleet operators

- Guyorguy Laguerre

- Apr 20

- 7 min read

Most fleet operators assume their standard commercial auto policy has them covered. It doesn’t. Motor carrier insurance is a legally distinct category with federal filing requirements, minimum liability thresholds, and coverage components that standard commercial auto simply doesn’t include. Miss one piece and you risk broker rejections, out-of-service orders, or catastrophic uninsured losses. This guide breaks down every layer of motor carrier insurance, from the core coverages to FMCSA compliance rules, so you can make informed decisions that protect your fleet, your contracts, and your operating authority.

Table of Contents

Key Takeaways

Point | Details |

Comprehensive coverage | Motor carrier insurance combines several coverages essential for truck fleets’ safety and compliance. |

Regulatory compliance | Federal and state laws set minimum insurance requirements and filings every fleet must understand. |

Custom selection | Tailor your insurance components and limits to your specific cargo, operations, and broker demands. |

Avoid costly gaps | Review policies and endorsements carefully to prevent uncovered exposures. |

Motor carrier insurance defined: What it covers and who needs it

Motor carrier insurance is a specialized form of commercial insurance designed specifically for entities that transport goods or passengers for hire across public roads. Unlike a standard commercial auto policy, which covers vehicles owned by a business, motor carrier insurance is built around the unique risks of for-hire trucking: third-party liability on public roads, cargo in transit, and regulatory compliance with federal and state agencies.

If you hold a USDOT number and operate as a for-hire carrier, you are legally required to carry this coverage. That includes truckload carriers, less-than-truckload (LTL) operations, freight brokers who also carry, and intermodal operators. Even private carriers transporting their own goods across state lines may face federal requirements depending on the commodity and weight class.

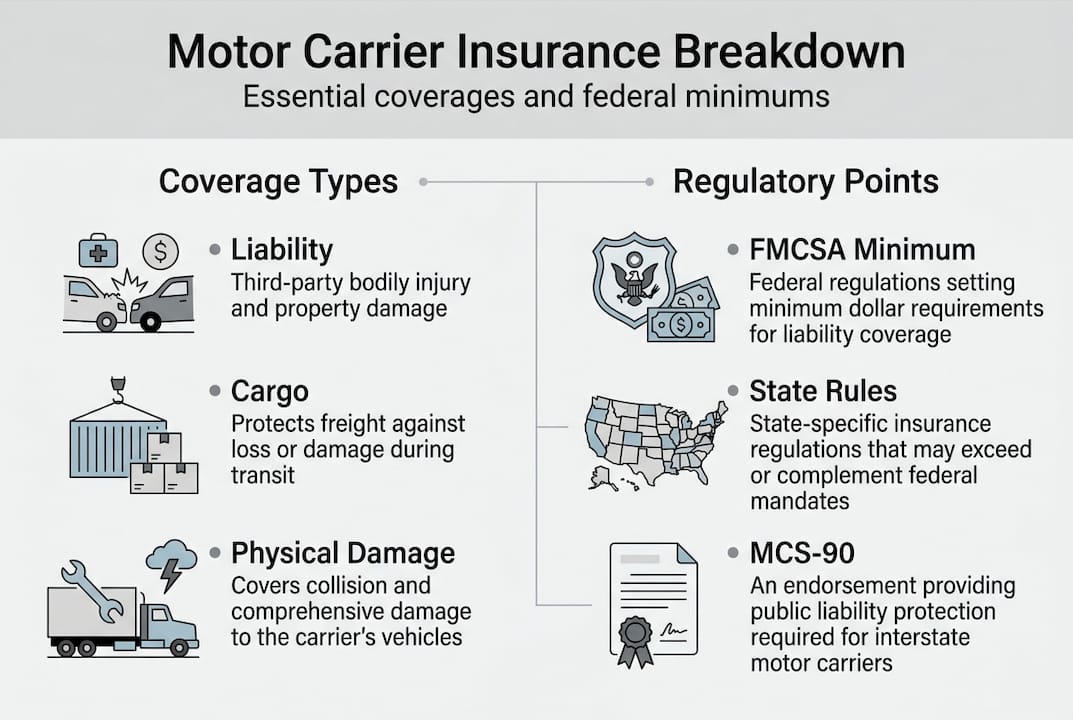

The foundation of trucking insurance essentials is understanding that motor carrier insurance isn’t one policy. It’s a structured suite of coverages, each addressing a specific exposure. As mandated by FMCSA and 49 CFR Part 387, the core components include:

Public liability: Covers bodily injury and property damage to third parties caused by your vehicles

Cargo insurance: Protects the freight you’re hauling against loss or damage in transit

Physical damage: Covers your own trucks and trailers for collision, fire, theft, and other perils

Bobtail and non-trucking liability: Covers your truck when it’s operating without a trailer or outside dispatch

General liability: Covers premises and operations liability not tied to vehicle use

The FMCSA sets federal minimums, but many shippers, brokers, and state agencies require limits well above those floors. Knowing commercial truck insurance basics is the starting point, but understanding the regulatory framework is what keeps your authority intact.

Key stat: FMCSA-regulated carriers hauling non-hazardous freight in vehicles over 10,001 lbs must carry a minimum of $750,000 in public liability coverage. Hazardous materials operations can require up to $5,000,000.

Breakdown of key motor carrier insurance coverages

Motor carrier insurance is a suite of coverages, each protecting against specific risks and liabilities. Here’s what each one actually does in practice.

Coverage type | What it protects | Who typically requires it | When it applies |

Public liability | Third-party injury and property damage | FMCSA, state agencies | Any at-fault accident on public roads |

Cargo insurance | Freight in transit | Shippers, brokers, FMCSA (some ops) | Loss, theft, or damage to cargo |

Physical damage | Your own trucks and trailers | Lenders, lessors | Collision, fire, theft, weather |

Bobtail liability | Truck operating without trailer | Leased owner-operators | Off-dispatch or deadhead moves |

General liability | Non-vehicle premises and ops risk | Shippers, terminals | Slip-and-fall, loading dock incidents |

To decide which coverages to prioritize for your operation, work through this process:

Identify your haul type and commodity. Hazmat, refrigerated, and high-value electronics each carry different cargo risk profiles and may trigger higher minimum requirements.

Review your contracts. Broker and shipper agreements often specify coverage types and minimum limits that exceed FMCSA floors.

Assess your fleet structure. If you use owner-operators under lease, bobtail insurance explained becomes critical because your primary policy typically doesn’t cover them off-dispatch.

Check state-specific overlays. Some states impose additional requirements beyond federal minimums.

Evaluate your physical assets. If you’re financing trucks or trailers, lenders will require physical damage coverage regardless of federal rules.

Pro Tip: Never assume a blanket policy covers all your exposures. Review each contract and commodity type separately. A single uninsured load of pharmaceuticals or electronics can exceed your entire annual premium budget in one claim.

Regulatory requirements and compliance: FMCSA and beyond

Compliance isn’t optional, and the consequences of getting it wrong are immediate. Brokers run carrier compliance checks before tendering loads. A lapsed filing or insufficient limit means no freight, no revenue.

The FMCSA sets public liability minimums under 49 CFR Part 387, and FMCSA filings and cargo limits must match your operation type. For most for-hire carriers, the required filings include Form BMC-91 or BMC-91X for public liability and Form BMC-34 for cargo insurance when required. These filings must be submitted directly by your insurer to FMCSA, not by you.

Operation type | Minimum public liability | Cargo filing required | Key form |

Non-hazmat, over 10,001 lbs | $750,000 | No (unless freight forwarder) | BMC-91/91X |

Hazmat (certain commodities) | $1,000,000 | Situational | BMC-91/91X |

Oil/hazmat (highest risk) | $5,000,000 | Situational | BMC-91/91X |

Household goods carriers | $750,000 | Yes | BMC-91/91X + BMC-34 |

One of the most misunderstood elements of motor carrier compliance is the MCS-90 endorsement. This is an attachment to your liability policy that acts as a financial guarantee to the public. As noted in trucking legal analysis, the MCS-90 endorsement guarantees public compensation to federal minimums, but carriers risk reimbursement to the insurer for excluded policy events.

What that means in plain terms: if an accident occurs during an activity your policy excludes, your insurer may still pay the injured party under MCS-90, but then come back to you for full reimbursement. That’s not a safety net. That’s a deferred liability.

State requirements add another layer. California, New York, and Illinois, among others, impose limits or filing requirements that go beyond federal floors. If you operate across multiple states, your insurance compliance tips strategy must account for the most stringent jurisdiction you operate in. Monitoring your trucking safety scores also matters here because poor CSA scores can trigger increased scrutiny and affect your insurability.

How to evaluate motor carrier insurance: Costs, risk, and selection tips

Once you understand what you need, the next challenge is getting the right coverage at a manageable cost. Premiums for motor carrier insurance vary widely based on several factors:

Fleet size and vehicle type: Larger fleets with heavier equipment carry higher base premiums, though volume can sometimes improve per-unit rates

Haul type and commodity: High-value or hazardous cargo significantly increases premium exposure

Driver history and safety record: Carriers with clean MVRs and strong CSA scores pay less. Period.

Loss history: Prior claims, especially at-fault accidents, drive premiums up sharply

Deductible choices: Higher deductibles reduce premiums but increase out-of-pocket risk per incident

Operating radius: Long-haul interstate operations carry more exposure than regional or local runs

To keep costs manageable, lower trucking insurance premiums by investing in driver training programs, dashcam systems, and regular vehicle maintenance. Insurers reward documented safety culture with better rates.

When comparing quotes, don’t just look at the premium number. Verify that FMCSA filings are included, confirm cargo limits match your maximum load values, and check exclusions carefully. Fleet operators should match FMCSA filings and cargo limits to their maximum load values and commodities to avoid broker rejections.

Pro Tip: Get best truck insurance quotes from carriers who specialize in commercial trucking, not general commercial lines insurers who dabble in it. Specialty markets understand your risk profile and write policies that actually fit your operation.

Common mistakes to avoid: letting filings lapse during policy renewals, underinsuring cargo to save on premium, and failing to update coverage when adding new commodities or expanding into new states. Each of these can result in denied claims or lost contracts.

A fleet operator’s perspective: What most guides miss about motor carrier insurance

Most insurance guides tell you what to buy. Few tell you what actually goes wrong.

The operators who get hurt aren’t usually the ones who skipped insurance entirely. They’re the ones who bought the minimum, checked the compliance box, and assumed they were covered. Then a refrigerated load spoiled in transit, or a driver operated the truck after hours for a personal errand and caused an accident, and suddenly they discovered their policy had exclusions they never read.

Relying on minimums creates a false sense of security. The FMCSA floor is a legal threshold, not a business protection strategy. Shippers and brokers increasingly require limits well above those floors, and a single large cargo claim can exceed your policy limits if you haven’t matched coverage to actual load values.

The other thing most guides skip: commercial truck insurance insights reveal that coverage gaps often appear at the edges of operations, during driver transitions, equipment changes, or new lane expansions. Those are the moments to review your policy, not after a loss. The operators who manage risk well treat insurance as an active business tool, not a passive compliance requirement.

Protect your fleet with the right motor carrier insurance partner

You now understand the structure, the compliance obligations, and the real-world risks that motor carrier insurance is designed to address. The next step is making sure your coverage actually matches your operation.

At Insuaria, we specialize in tailored motor carrier insurance solutions for fleet operators and logistics companies. From FMCSA filings to high-limit cargo policies, we help you build coverage that fits your haul type, your fleet size, and your growth plans. Explore our truck insurance coverage details or request a customized quote today. Don’t leave your operating authority and your cargo exposed to gaps that a well-structured policy could close.

Frequently asked questions

Is motor carrier insurance required by federal law?

Yes, FMCSA requires carriers to maintain minimum public liability insurance under 49 CFR Part 387, with specific cargo filing requirements depending on operation type.

What does an MCS-90 endorsement do?

The MCS-90 ensures injured parties receive compensation up to federal minimums even for excluded events, but the insurer can seek reimbursement from the carrier for those excluded incidents.

How can I keep my motor carrier insurance costs down?

Improve driver safety records, invest in fleet safety technology, and match cargo limits to your actual operation type rather than defaulting to minimum required values.

Can one policy cover all my trucking risks?

No. Motor carrier insurance includes multiple coverages addressing distinct risks, and most policies are modular, requiring you to select and combine the right components for your specific operation.

Recommended

Comments