Navigate the Truck Insurance Claims Process with Confidence

- Guyorguy Laguerre

- May 14

- 12 min read

TL;DR:

Proper documentation and timely reporting are critical to a smooth trucking insurance claim process. Gathering evidence such as police reports, photos, witness contacts, repair estimates, and electronic data within the first 15 minutes helps prevent delays and denials. Following a structured step-by-step process, maintaining consistent statements, and actively managing investigations can significantly shorten settlement times and improve outcomes.

You’re parked on the shoulder of I-80 after a collision, your rig is damaged, freight may be compromised, and you have no idea what to do next. That helpless feeling is where most truck insurance claims go wrong. Delays and outright denials happen every day, not because drivers did anything criminal, but because they simply didn’t know what to document, when to report, or how to communicate with their insurer. This guide walks you through every stage of the truck insurance claims process so you can act with clarity, submit with confidence, and avoid the costly mistakes that drag claims out for months.

Table of Contents

What to gather before filing: Documentation and evidence checklist

Step-by-step: How to file a truck insurance claim efficiently

How insurer investigations work: Electronic evidence, coverage, and timing realities

Avoiding delays and denials: Common mistakes and troubleshooting tips

The best-kept secrets for faster, smoother truck insurance claims

Key Takeaways

Point | Details |

Complete documentation upfront | Submitting a full packet of evidence from day one minimizes delays. |

Act fast after the incident | Filing within 24–48 hours boosts your credibility and claim success. |

Stay consistent and responsive | Prompt communication and matching your story to the evidence speeds up claim resolutions. |

Know the real timelines | Plan for your settlement to take months, not weeks. |

What to gather before filing: Documentation and evidence checklist

Having previewed what you’ll gain, let’s start by breaking down exactly what you need to gather before touching any paperwork.

The moment an incident happens, your claim’s outcome is already being shaped by the evidence you collect or fail to collect. Insurers don’t just take your word for what happened. They compare your account against physical evidence, third-party reports, and digital data. The good news is that submitting a complete documentation packet with your initial claim, rather than sending documents piece by piece, significantly reduces back-and-forth delays and keeps your claim moving forward.

Here’s what a complete documentation packet looks like for a commercial truck claim:

Police report: Always get the official report number at the scene and request a copy as soon as it’s available. This is the foundation of your claim.

Photos and video: Capture every angle of vehicle damage, road conditions, skid marks, signage, and the surrounding scene. Wide shots and close-ups both matter.

Witness contact information: Names and phone numbers of anyone who saw the incident. Independent witnesses carry more weight with adjusters than you might expect.

Repair and towing estimates: Get written estimates from qualified repair shops. If your rig was towed, document that cost separately with a receipt.

Medical records: For any injury, even a seemingly minor one, document the evaluation from a healthcare provider. This creates a direct, timestamped link between the incident and the injury.

A written incident description: Write a clear, factual narrative of what happened. Stick to what you know and observed directly.

ELD and telematics data: For commercial trucks, electronic logging device records and black-box data are increasingly central to fault determination. Pull and preserve this data immediately.

Document type | Why it matters | When to collect |

Police report | Official, neutral record of the incident | At the scene and follow up within 24 hours |

Photos and video | Visual proof of damage and conditions | Immediately at the scene |

Witness info | Supports your account independently | Before leaving the scene |

ELD/telematics data | Establishes speed, route, and behavior | Within hours. Data can be overwritten |

Repair estimates | Quantifies the financial loss | Within 48 hours of the incident |

Medical records | Links injuries to the incident | Same day or following morning |

For owner-operators and fleet managers, the digital trail from your truck’s onboard systems is often the most powerful evidence you have. Review your trucking company insurance tips to understand how documentation connects to your specific policy type. If you manage multiple vehicles, your fleet insurance coverages may have additional documentation requirements per unit. And if your claim involves lost or damaged freight, the terms of your cargo insurance guide will dictate what additional records you need for that portion of the claim.

Pro Tip: The best time to start your documentation is within the first 15 minutes at the scene, before vehicles are moved and before weather or traffic changes the physical evidence. Set a mental trigger: incident happens, phone comes out.

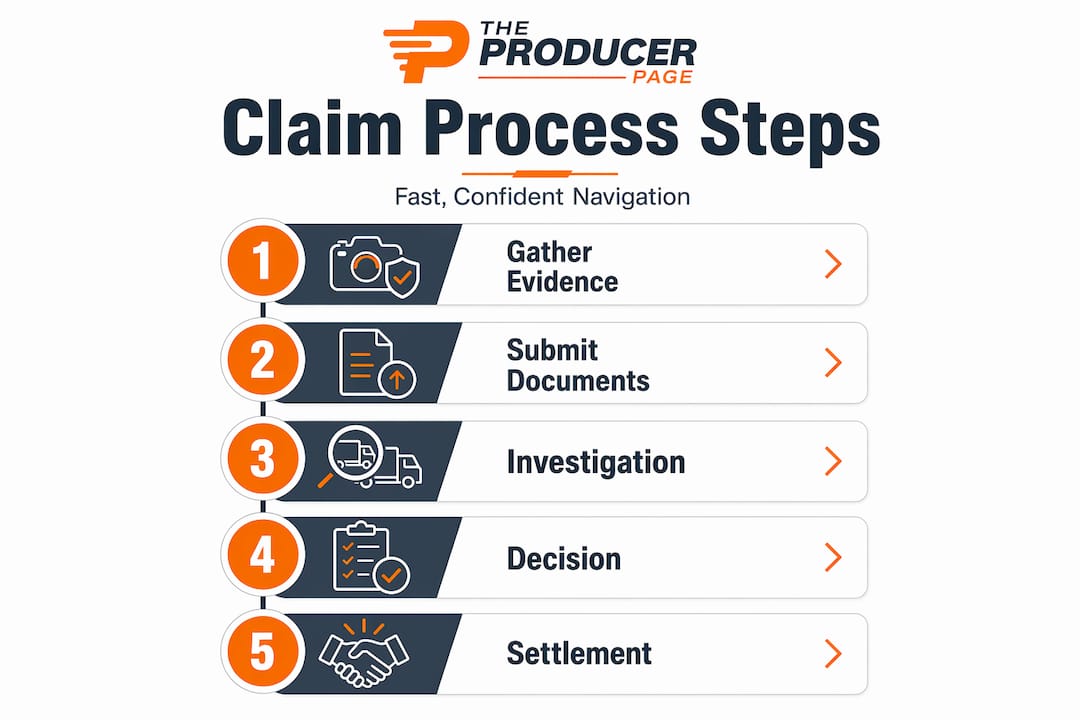

Step-by-step: How to file a truck insurance claim efficiently

With your evidence in hand, it’s time to put the process in motion. Here’s how to file step by step.

The U.S. truck claims process follows a consistent baseline workflow, and understanding each step removes a lot of the anxiety that leads people to make hasty, costly mistakes.

Prioritize safety and medical attention first. Move vehicles out of traffic if possible and check for injuries. Call 911 and wait for law enforcement to arrive. Do not skip this step even if the damage looks minor.

Report to law enforcement and get documentation. Make sure a police report is filed and get the officer’s badge number and report number. This creates the official record.

Notify your insurer promptly. Call your insurance carrier or broker as soon as it is safe to do so. Most policies require prompt notice, and waiting even a day or two can create complications.

Submit your complete documentation packet. Don’t wait until everything is perfect. Submit what you have and flag what is still pending, such as the official police report or a second repair estimate.

Work with your assigned adjuster. Once your claim is opened, you’ll be assigned an adjuster who manages the investigation. Respond to every request quickly and keep a log of all communications.

Cooperate with the investigation. The insurer will compare your narrative, the police report, ELD data, and any third-party statements. Be consistent, honest, and thorough.

Receive the coverage determination and settlement. Once the investigation concludes, the insurer determines liability and coverage, then issues payment or explains a denial.

“The single most important thing you can do after a truck accident is not let urgency push you into rushing or omitting key documentation. A slow, complete submission will almost always beat a fast, incomplete one.”

Here’s a side-by-side comparison of how an organized submission plays out versus a disorganized one:

Scenario | Organized submission | Disorganized submission |

Documentation | Complete packet submitted upfront | Documents sent one at a time over weeks |

Adjuster communication | Responsive and consistent | Delayed replies and changing statements |

Investigation duration | Shorter, fewer follow-up requests | Longer, multiple clarification rounds |

Claim outcome | Faster resolution and clearer settlement | Potential delays, disputes, or denial |

Your commercial trucking insurance overview is a useful reference point for understanding what your specific policy covers before the adjuster starts asking questions. The more familiar you are with your own coverage, the more effectively you can communicate during the claims process.

How insurer investigations work: Electronic evidence, coverage, and timing realities

Once your claim is submitted, here’s what actually happens behind the scenes during the insurer’s investigation.

Most truck owners assume the insurer just reviews photos and the police report. The reality is considerably more complex, especially for commercial operations. Electronic evidence from ELD systems, telematics devices, and onboard black boxes is routinely used to reconstruct what happened and establish fault. This data can confirm your speed, braking patterns, hours of service compliance, and the exact GPS route you traveled.

Here’s what the insurer’s investigation team is typically looking at:

Your written statement vs. ELD data: Does your account of speed and braking match what the device recorded?

Police report vs. witness statements: Are the accounts consistent, or are there contradictions that need resolution?

Hours of service records: Were you compliant with FMCSA driving hour limits at the time of the incident?

Maintenance records: Was the truck properly maintained? Outstanding mechanical issues can affect coverage decisions.

Cargo manifests: For freight claims, what was loaded, how was it secured, and was it declared correctly?

On the regulatory side, FMCSA filings and active coverage must be correctly aligned for your claim to proceed without a coverage dispute. If your operating authority is current but your insurance filings have lapsed or don’t meet federal minimums, the insurer can raise a coverage challenge that stalls your claim entirely. Check your policy’s effective dates, make sure your BMC filings are current, and confirm that your coverage meets the minimum requirements for your type of operation before you ever need to file.

Investigation element | What the insurer checks | Risk if missing or inconsistent |

ELD data | Speed, braking, hours of service | Fault determination or compliance issue |

Maintenance records | Scheduled and completed repairs | Equipment failure liability |

FMCSA filings | Active policy and federal minimums | Coverage dispute or denial |

Witness statements | Independent account of incident | Contradiction with driver’s narrative |

Cargo documentation | Load type, weight, securement | Separate cargo claim complications |

For fleet operators, keeping your fleet insurance explained documentation aligned with your FMCSA records is not just good practice, it’s the difference between a smooth claim and a protracted legal dispute.

Pro Tip: Pull your ELD data yourself before submitting a claim. Knowing exactly what it shows allows you to address any discrepancies in your written narrative proactively, rather than having an adjuster discover them and start asking hard questions.

Avoiding delays and denials: Common mistakes and troubleshooting tips

With an understanding of what insurers scrutinize, let’s now focus on what causes headaches and how you can avoid them.

Most truck insurance claim delays and denials are preventable. The leading causes are late reporting, incomplete documentation, and inconsistent statements. These aren’t rare edge cases. They happen regularly, even to experienced owner-operators who have filed claims before.

Here are the most critical mistakes to avoid:

Filing late: Most policies require you to report an incident within a specific window, often 24 to 72 hours. Late filing gives the insurer grounds to question your credibility and can even void coverage depending on your policy language.

Submitting incomplete documentation: Missing a repair estimate or forgetting to include medical records forces the adjuster to send follow-up requests, each of which adds time to your claim.

Admitting fault prematurely: Never admit fault to the other party, law enforcement (beyond factual statements), or your insurer until liability has been formally determined. Even a casual “I should have braked sooner” can become a documented admission.

Ignoring adjuster requests: When your adjuster asks for additional information, respond within 24 hours if possible. Delayed responses are often interpreted as lack of cooperation and can pause your claim.

Inconsistent statements: If your written narrative says one thing and your verbal statement to the adjuster says another, it raises red flags. Write your incident description immediately while details are fresh and stick to it.

Failing to document ongoing impacts: If your truck is out of service for repairs, document every day of lost revenue. These records support your claim for business interruption or lost income, if your policy includes that coverage.

Pro Tip: Keep a dedicated claims folder, physical or digital, where you store every document, email, and phone log related to the incident. If your claim is ever disputed, this record becomes your most valuable asset.

Learning to reduce trucking insurance costs through good claims history starts with knowing how to handle claims correctly when they arise. And if you’re working through a broker, understanding how insurance brokers for fleets advocate for you during a claim can make a meaningful difference in the outcome.

How long does the truck claims process really take?

Knowing how to avoid pitfalls, you also need to set your expectations. Here’s the reality on how long the process might take.

Most truck accident claim settlements take between 3 and 18 months. That’s not a typo. Settlement timelines for truck claims are significantly longer than standard auto claims because the investigations are more complex, the dollar amounts are larger, and liability often involves multiple parties including the driver, the carrier, the cargo owner, and sometimes a third-party maintenance vendor.

Several factors directly influence where your claim falls in that 3 to 18 month range:

Injury severity: Claims with significant injuries involve medical evaluations, specialist opinions, and sometimes long-term care assessments. Insurers won’t settle until the full extent of injuries is established, which takes time.

Liability complexity: When multiple parties are involved, each insurer conducts its own investigation. Reconciling three or four separate findings takes months even when everyone is cooperating.

Documentation completeness: Complete, organized submissions consistently resolve faster. Incomplete claims cycle through rounds of requests and responses that stretch timelines significantly.

Coverage disputes: If your FMCSA filings aren’t current or your policy has coverage gaps, the insurer may dispute their obligation entirely. These disputes can trigger legal proceedings that extend timelines well beyond 18 months.

Negotiation complexity: Large settlements involving significant property damage, cargo loss, and personal injury don’t resolve in a single offer. Multiple rounds of negotiation are common.

While your claim is being processed, here’s what you should be doing:

Check in with your adjuster every two weeks. Keep the communication line open without being intrusive.

Document all ongoing losses, including rental costs, lost loads, and missed contracts.

Update your insurer immediately if new information emerges, such as a delayed injury diagnosis.

Consult with a licensed professional if you believe your claim is stalled without valid reason.

Avoid signing any release forms until you fully understand what rights you are waiving.

Patience matters here, but passive patience doesn’t. Stay actively informed and keep records of every interaction.

The best-kept secrets for faster, smoother truck insurance claims

After laying out the system in full, it’s worth stepping back and sharing what actually separates the claims that resolve quickly from the ones that drag on indefinitely.

The first truth is uncomfortable: most slow claims are the claimant’s fault, not the insurer’s. That’s not a knock on truck owners. It’s a reflection of how little formal preparation most people receive before an incident happens. The first 24 to 48 hours after a crash are the highest-leverage period in the entire claims process. What you do in that window shapes everything that follows. Police involvement, scene photographs, witness contacts, and same-day insurer notification are not optional best practices. They are the foundation of a winnable claim.

The second truth is that insurers are not adversaries, but they are trained observers. They look for consistency across every document, statement, and data point. A small inconsistency between your written narrative and your ELD timestamp can turn a straightforward claim into a six-month investigation. This isn’t about catching you in a lie. It’s about verifying that the story holds together. The truck owners who understand this tend to write clearer, more careful incident narratives and come to adjuster calls fully prepared.

The third truth is about injuries. Even if you feel unhurt immediately after a crash, get a medical evaluation the same day. Adrenaline masks pain. Symptoms from whiplash, soft tissue injuries, and even mild concussions often don’t surface until 24 to 48 hours later. If you don’t have a medical record from around the time of the incident, proving that your injury resulted from that specific crash becomes genuinely difficult. Insurers and opposing counsel will argue that the gap in documentation suggests the injury occurred somewhere else.

Finally, treat your documentation like a legal filing, not a casual summary. Every detail you record at the scene is a potential asset. Every detail you omit is a potential liability. Trucking professionals who approach claims with the same discipline they bring to load planning and route compliance consistently see faster resolutions and better outcomes.

To get organized before an incident occurs, visit the trucking intake page and see how you can prepare your coverage information in advance.

Insuaria makes truck claims and coverage simpler

With these insights in hand, here’s how Insuaria can further simplify and support your insurance and claims needs.

Filing a truck insurance claim is stressful enough without also trying to figure out which documents go where, which agency to call, or how to present your coverage details to a licensed professional. Insuaria was built to remove that friction. Our intake platform helps truck owners and fleet operators organize the information that licensed insurance professionals need to review your coverage situation efficiently.

Whether you’re an owner-operator looking to review your current truck insurance options or a fleet manager needing to get your documentation organized for a coverage review, Insuaria gives you a clean, structured way to submit your details. You can also use our digital claims file share tool to securely upload and organize your incident documents before a licensed agency partner follows up. For companies managing multiple trucks and drivers, our business insurance intake makes it easier to present your fleet’s full picture. Insuaria doesn’t issue quotes or bind coverage, but we make sure you arrive at that conversation prepared.

Frequently asked questions

What documents do I need to provide when filing a truck insurance claim?

You must provide the police report, accident photos, witness information, repair and towing estimates, and any medical records for injuries. A complete documentation packet submitted upfront significantly reduces delays and back-and-forth with the adjuster.

How soon after a truck accident should I file an insurance claim?

File your claim as soon as possible, ideally within 24 to 48 hours of the incident, after ensuring safety and medical attention. The first 48 hours are the highest-leverage period for securing evidence and establishing your credibility with the insurer.

What is the average timeline for a truck insurance settlement?

Truck accident claim settlements typically take between 3 and 18 months, depending on injury severity, liability complexity, and how complete your documentation was at submission.

What is FMCSA and why does it matter for claim approval?

FMCSA (Federal Motor Carrier Safety Administration) requires certain truck operators to maintain active insurance filings that meet federal minimums. If those filings are lapsed or misaligned with your operating authority, the insurer can raise a coverage dispute that stalls or denies your claim.

What are the top reasons truck insurance claims get delayed or denied?

The main causes are late filing, incomplete documentation, inconsistent statements across reports and conversations, and failure to respond promptly to adjuster requests.

Recommended

Comments