Optimize Your Fleet: Progressive Trucking Insurance Guide

- Guyorguy Laguerre

- May 13

- 11 min read

TL;DR:

Many trucking owners mistakenly believe a commercial auto policy fully covers their needs, risking significant financial exposure. Progressive’s modular coverages allow customized protection based on operational specifics, helping fleets stay compliant and avoid costly gaps. Tailoring coverage limits, understanding endorsements, and strict claims management are essential for long-term risk mitigation and business continuity.

Many trucking business owners assume that once you have a commercial auto policy, you’re covered. That assumption can cost you everything. Progressive’s modular commercial auto coverages let you select specific protection types, limits, and deductibles rather than accepting a generic bundle someone else designed. This guide walks you through how to build smarter coverage, stay compliant with federal and state rules, and avoid the expensive gaps that sink even experienced fleets. Whether you run a single owner-operator rig or manage a growing fleet, understanding your options is the first step toward real protection.

Table of Contents

Key Takeaways

Point | Details |

Modular coverage options | Progressive lets you customize which trucking insurance coverages and limits fit your needs. |

Compliance and filings | Progressive supports FMCSA and state insurance requirements, so you stay compliant and operational. |

Importance of endorsements | Special endorsements like Cargo Plus protect your business against edge-case risks not covered by standard policies. |

Claims best practices | Prompt reporting and accurate documentation help you avoid delays or denied claims. |

Smart premium strategies | Lowest-cost policies may increase business risk—balance price with comprehensive protection. |

What makes Progressive trucking insurance unique?

Off-the-shelf coverage doesn’t cut it for trucking. The risks you face on the road depend on what you haul, where you drive, how many trucks you operate, and what kind of contracts you’re under. Progressive recognized this early, which is why their commercial truck program was designed around flexibility rather than fixed packages.

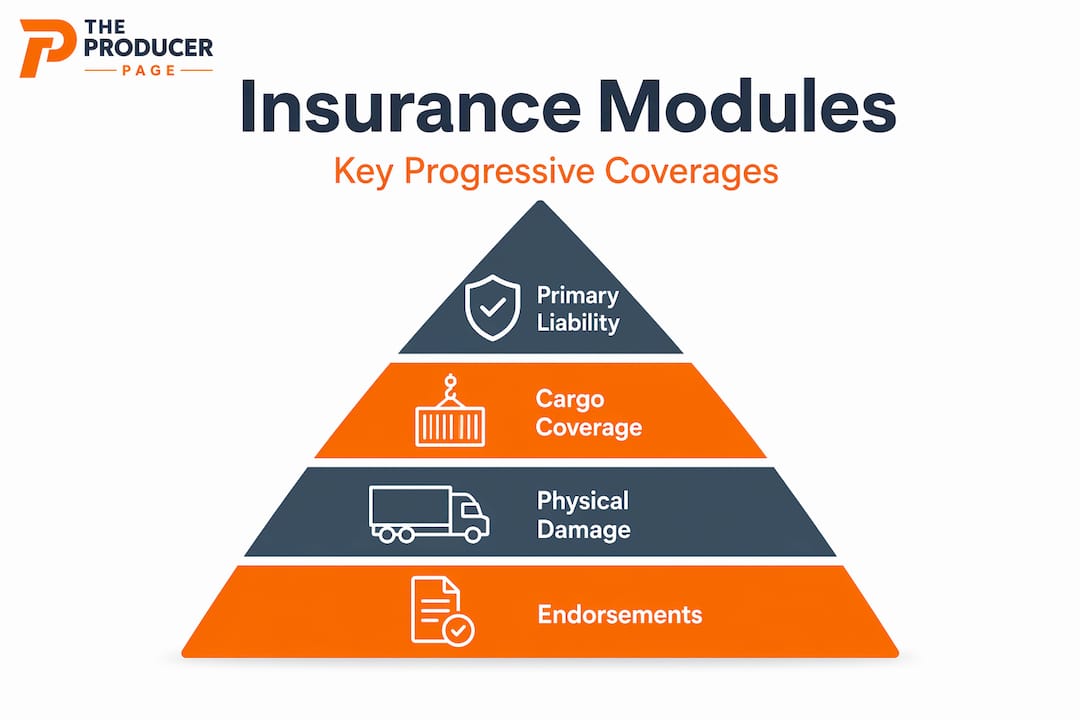

The truck insurance coverages offered by Progressive Commercial are built as individual modules. You choose what goes into your policy and at what level. That means you can pair primary liability with physical damage, add motor truck cargo, and include non-trucking liability if your drivers use trucks for personal errands. You’re not forced to pay for coverages that don’t apply to your operation.

Here’s a quick overview of the core coverage types and what each one actually does:

Coverage Type | What It Covers | Who Needs It Most |

Primary liability | Injuries and property damage to others | All commercial carriers |

Physical damage | Your truck (collision and comprehensive) | Owner-operators with financed rigs |

Motor truck cargo | Freight you’re hauling if it’s damaged or stolen | Any carrier transporting goods |

Non-trucking liability | Coverage when the truck is used off-dispatch | Leased owner-operators |

Trailer interchange | Damage to non-owned trailers under a written agreement | Drivers using leased trailers |

Rental reimbursement | Temporary vehicle costs after a covered loss | Fleets that can’t afford downtime |

Towing and roadside | Emergency breakdown assistance | Owner-operators and small fleets |

This kind of modular setup gives you real control. For owners running fleet insurance options, this flexibility is especially valuable because your exposure changes as you add trucks, routes, and freight types.

A few coverage highlights worth knowing:

Non-trucking liability is often misunderstood. It’s not the same as bobtail insurance, though people use the terms interchangeably. It specifically covers drivers who are under a permanent lease to a motor carrier but are operating the truck for non-business purposes.

Trailer interchange requires a written trailer interchange agreement to be active. Without that agreement on file, damage to a borrowed trailer may not be covered.

Motor truck cargo covers the freight itself, not your truck. If a load of electronics is damaged in an accident, cargo coverage handles the shipper’s claim against you.

Understanding liability coverage explained in the context of trucking is critical before you configure your policy.

Pro Tip: Don’t treat your policy like a buffet where you grab whatever sounds good. Build it around your specific operations. If you’re a dry van carrier running the Midwest, your risk profile is very different from a tanker operator on coastal routes. Customize accordingly.

A notable industry figure: over 500,000 trucking companies operate in the U.S., and the vast majority are small carriers running six trucks or fewer. These smaller operations often have the most to lose from poorly structured coverage because they lack the financial reserves to absorb a major uninsured loss.

How to choose coverage types, limits, and deductibles

Understanding the menu of options is step one. Making smart choices for your business risk and budget is where the real work begins.

Every coverage decision involves two key numbers: the limit and the deductible. The cargo limit you select determines the maximum Progressive will pay on a cargo claim, while the deductible is what you pay out of pocket before coverage kicks in. Higher deductibles lower your premium but increase your financial exposure when something goes wrong. That trade-off sounds simple, but it trips up a lot of operators who optimize for monthly cost instead of total risk.

When it comes to primary liability coverage, underwriting factors that shape your rate include truck type, cargo, driving history, location, drivers, number of trucks, coverage limits, and deductibles. This means two fleets with identical truck counts can have dramatically different premiums based on where they operate and what they carry.

Here’s how those factors break down in practice:

Underwriting Factor | Lower Risk Profile | Higher Risk Profile |

Truck type | Light commercial trucks | Heavy semis, tankers, flatbeds |

Cargo | Dry goods | Hazmat, oversized loads, perishables |

Driving history | Clean records, experienced drivers | Recent violations, new CDL holders |

Location | Rural, low-traffic routes | Urban corridors, high-accident states |

Fleet size | Smaller, stable fleets | Rapid growth with new drivers |

Use this numbered checklist when selecting or adjusting your coverage each policy period:

Identify your mandatory minimums. Know what the FMCSA and your state require before adding anything else. These are your floor, not your ceiling.

Assess your cargo value. If you regularly haul freight worth $150,000 per load, a $50,000 cargo limit leaves you dangerously exposed.

Evaluate your deductible capacity. Ask yourself honestly: if you had to pay your deductible tomorrow, could your business absorb that cost without disruption?

Review your driver roster. New or young drivers with limited experience increase liability exposure. Factor that into your limits.

Check your contractual requirements. Many brokers and shippers require specific insurance minimums in their contracts. If you don’t meet them, you can’t haul for them.

Consider your downtime tolerance. If losing a truck for two weeks would cripple your cash flow, rental reimbursement coverage may be worth the added cost.

Revisit annually. Your business changes. So should your coverage. Growth, new routes, and added equipment all shift your risk profile.

The right approach to choosing insurance limits involves thinking about worst-case scenarios, not just average claims. One nuclear verdict can end a trucking business that carries inadequate limits.

For help with reducing trucking insurance costs without sacrificing essential protection, focus on driver safety programs, telematics data, and claims history before touching your coverage structure.

Pro Tip: A surprisingly low premium is almost always a red flag. Either the coverage limits are too low to protect you, the deductibles are sky-high, or some critical coverage is missing entirely. Read the policy, not just the price.

Compliance essentials: Meet federal and state requirements

Once you’ve mapped your coverage, compliance is critical to stay on the road legally and avoid costly mistakes.

Federal law sets a baseline that every interstate motor carrier must meet. The FMCSA mandates minimum insurance coverages for motor carriers operating on public roadways, and states can impose additional requirements on top of those federal floors. Operating without proper coverage isn’t just a business risk. It’s a legal one that can result in your authority being revoked.

Here’s what compliance looks like at a high level:

Primary liability minimum: $750,000 for most freight haulers under FMCSA regulations. Hazmat carriers typically need $1 million or more.

State-specific filings: Many states require proof of insurance on file with state transportation agencies. These filings (commonly called Form MCS-90 or state equivalents) prove you meet minimum requirements.

BMC-91 filings: Required by the FMCSA for licensed carriers. This form certifies your insurance meets federal standards.

Operating authority maintenance: Your MC number can be suspended if insurance lapses, even temporarily.

Progressive Commercial supports trucking-specific coverages plus federal and state filings, along with 24/7 heavy-truck claims handling with in-house adjusters. Having an insurer who manages these filings directly removes a major administrative burden from your operation.

For a deeper look at your obligations, a solid motor carrier compliance guide can help you map out exactly what filings your operation requires.

One of the most alarming facts in trucking compliance right now:

“Verdicts exceeding $100 million in 2023 reached a record high, and the federally mandated minimum insurance requirement has remained unchanged since 1985 at $750,000.” FleetOwner

Think about that for a moment. The minimum was set in 1985, when the cost of a serious injury claim was a fraction of what it is today. A carrier relying on bare-minimum coverage in today’s litigation environment is carrying a loaded financial risk with almost no cushion. Attorneys who specialize in trucking accidents know exactly how to target underinsured carriers. Don’t make yourself an easy target.

State requirements are equally important to track. Some states require additional uninsured motorist coverage. Others have specific endorsements tied to intrastate commerce. If you’re running loads across state lines, you need to understand the rules in every state where your trucks operate, not just where they’re registered.

Nuanced coverages and endorsements: Cargo Plus and more

Covering the basics is essential, but special industry risks demand next-level solutions. That’s where endorsements like Cargo Plus fit in.

In April 2025, Progressive made a significant announcement for freight carriers dealing with specialty loads. The Cargo Plus endorsement expands Motor Truck Cargo coverage to include perils attributed to wetness, rust, and corrosion. It also covers driver-error and temperature-change-related perils on refrigerated loads for customers who purchase Refrigeration Breakdown coverage.

Why does this matter? Standard cargo insurance has gaps that most carriers don’t discover until they file a claim and get denied. Consider these real-world scenarios:

A flatbed carrier hauls steel coils through heavy rain. The cargo arrives with rust damage. Standard cargo coverage may exclude corrosion. Cargo Plus fills that gap.

A refrigerated carrier’s reefer unit fails due to driver error. The load of frozen seafood is lost. Without the Cargo Plus endorsement, that claim could be denied.

A produce carrier hauls fresh strawberries in summer. A temperature spike during transit damages the load. Temperature-related perils without Refrigeration Breakdown coverage often fall outside standard policies.

For specialized coverage options that address these freight-specific risks, working with a knowledgeable insurance professional is essential. The right endorsement can mean the difference between a fully paid claim and a six-figure loss that comes directly out of your operating capital.

Here’s a comparison of standard cargo coverage versus the Cargo Plus enhancement:

Standard motor truck cargo: Covers physical damage from accidents, theft, and listed perils. Excludes many moisture, temperature, and corrosion-related losses.

Cargo Plus endorsement: Adds wetness, rust, and corrosion perils. Adds temperature-change events on refrigerated loads when paired with Refrigeration Breakdown coverage.

Who benefits most: Flatbed operators, refrigerated carriers, produce haulers, and anyone moving high-value or moisture-sensitive freight.

Pro Tip: Before you assume a standard cargo policy covers your specific freight type, ask your licensed insurance professional to walk through your policy’s exclusions. The most expensive coverage gaps are the ones nobody told you about.

The specialty endorsement market in trucking is growing because the freight landscape is evolving. E-commerce has increased the volume of high-value, time-sensitive loads moving through the system. Carriers who haul these loads need coverage that keeps pace with their actual exposure.

Smooth claims handling: Getting the most from your policy

Even well-designed coverage only keeps you safe if you know how to handle accidents and claims correctly. Getting it wrong can turn a payable claim into a disputed one.

Here’s a step-by-step guide for handling a claim effectively:

Stop and secure the scene. Ensure driver safety first, then document the situation before anything moves or changes.

Capture complete evidence. Take photos of all vehicles, the road surface, cargo condition, weather, signage, and any visible damage. More is always better.

Get witness information. Names, phone numbers, and statements from anyone who saw the incident can be decisive.

Report promptly. Progressive’s claim guidance consistently emphasizes prompt accident reporting, completeness and accuracy of statements and evidence, and avoiding early admissions of fault.

Be accurate, not just fast. Rushing through a claim report with incomplete or incorrect information creates problems that are difficult to fix later.

Do not admit fault at the scene. This is not about being dishonest. It’s about letting the investigation determine facts rather than having a stressed, time-pressured driver make statements that could be taken out of context.

Keep a claims log. Document every conversation, every document submitted, and every response you receive. If a dispute arises, your records are your best asset.

Common mistakes that lead to denied or delayed claims include late reporting, inconsistent statements, missing documentation, and failing to notify the insurer before a damaged load is disposed of or repaired. Each of these issues gives the adjuster a legitimate reason to slow down or deny the process.

“The fastest way to protect a claim is to treat the first 48 hours like the most important documentation window of the entire event. Everything you capture in that window shapes how the claim is evaluated.” (Progressive claims guidance)

Progressive’s in-house adjusters who handle heavy-truck claims around the clock are a genuine operational advantage. Trucking doesn’t stop at 5 PM, and neither do accidents. Having an adjuster available at 2 AM when your driver is stranded with a damaged rig on I-80 is not a luxury. It’s a business necessity.

For more trucking insurance tips on documentation, driver training, and claims preparation, building these habits into your regular operations will pay dividends when the unexpected happens.

The real strategy: Why cheapest isn’t safest

Let’s step back and look at the broader strategy for insurance selection beyond just cost and compliance.

Here’s a perspective you won’t often hear from people trying to sell you a policy: the trucking owners who consistently protect their businesses over the long term don’t shop for insurance the same way they shop for diesel. They treat their coverage structure as an investment in business continuity, not a line item to minimize.

The real danger of a low-cost policy is what’s hiding behind that number. A premium that looks too good compared to competitors often conceals higher deductibles, stripped-down limits, missing endorsements, or exclusions buried in the fine print. You won’t know any of that until you file a claim and get a fraction of what you expected.

Understanding trucking premiums means looking beyond the monthly number and asking what happens in a worst-case scenario. What would a $2 million liability verdict cost you at your current limits? What would a $200,000 cargo loss cost you with a $50,000 limit and a $10,000 deductible? Do the math before you decide the cheaper policy is the smarter one.

Experienced fleet owners know something that newcomers learn the hard way: a single catastrophic claim on an underinsured fleet can wipe out years of premium savings in one afternoon. The math simply doesn’t favor minimizing coverage. What it does favor is building a policy structure that protects your revenue, your equipment, and your liability exposure so that one bad day doesn’t permanently alter your business trajectory.

The operators who prioritize comprehensive structure over minor monthly savings are not being reckless with money. They’re being precise with risk. And in trucking, that precision is exactly what separates the fleets that grow from the ones that don’t recover.

How Insuaria helps trucking businesses secure smarter insurance

Now that you know how smart coverage works, here’s how to put it into action for your fleet.

Building the right trucking insurance structure requires organized information, clear questions, and access to professionals who understand commercial freight risk. That’s exactly where Insuaria comes in. Our intake platform is built to simplify the first step of the insurance review process so you walk into that conversation prepared, not confused.

When you begin a trucking insurance intake, you’re organizing the details that licensed insurance professionals need to evaluate your coverage needs accurately. Fleet size, cargo types, routes, driver history, current coverage gaps — all of it documented clearly before a licensed agency partner follows up. You can also explore truck insurance information or streamline your business insurance process through our simple forms. Insuaria doesn’t bind coverage or issue quotes, but we make sure you’re ready for the conversation that does.

Frequently asked questions

What is the minimum trucking insurance required by law?

The FMCSA requires at least $750,000 in primary liability coverage for most interstate carriers, a figure that has not changed since 1985, though many experts recommend carrying significantly higher limits given today’s litigation environment.

Does Progressive trucking insurance cover refrigerated cargo?

Yes, Progressive’s Cargo Plus endorsement extends protection to cover temperature-change-related losses for refrigerated loads when the Refrigeration Breakdown coverage is also purchased, filling a critical gap in standard cargo policies.

What factors affect the price of Progressive trucking insurance?

Pricing is shaped by truck type, cargo, driving history, location, number of trucks, coverage limits, and chosen deductibles, meaning two carriers with the same fleet size can pay very different rates based on their specific operations.

How quickly does Progressive handle trucking insurance claims?

Progressive provides 24/7 heavy-truck claims support with in-house adjusters, which means you have access to a real claims professional any time an incident occurs, regardless of the hour or day.

Recommended

Comments