Reduce trucking insurance costs: proven fleet strategies

- Guyorguy Laguerre

- Apr 21

- 7 min read

Trucking insurance is one of the biggest line items eating into your fleet’s margin, and it keeps climbing. The good news is that 10-25% savings are achievable when you combine smarter shopping with disciplined safety and compliance programs. This guide walks you through exactly how to get there, step by step, without sacrificing the coverage that protects your business when things go wrong on the road.

Table of Contents

Key Takeaways

Point | Details |

Review all policies | Understanding your current coverage and claims history is key to avoiding costly mistakes. |

Use industry specialists | Specialist brokers typically save fleets 10–25% compared to generalists. |

Focus on safety scores | Improving CSA and ISS scores can directly lower premium rates. |

Leverage your data | Presenting strong safety and maintenance records leads to better insurance negotiations. |

Don’t sacrifice coverage | Cutting costs too aggressively may hurt long-term stability after a claim. |

Understand your current insurance and risk profile

Before you can cut costs, you need to know what you’re actually paying for and why. Many fleet operators skip this step and go straight to shopping for cheaper quotes, only to discover later they dropped critical coverage or missed a claims issue that’s quietly inflating their rates.

Start by pulling together these key documents:

Current policy declarations pages for every vehicle and liability line

Three to five years of claims history, including frequency and severity

CSA (Compliance, Safety, Accountability) scores from the FMCSA portal

ISS (Inspection Selection System) scores for each unit

Driver MVRs (Motor Vehicle Records) updated within the last 12 months

Once you have these in hand, look for patterns. Are claims concentrated in one driver or one route? Are your CSA scores trending up in a specific BASIC category? These patterns tell you where to focus first.

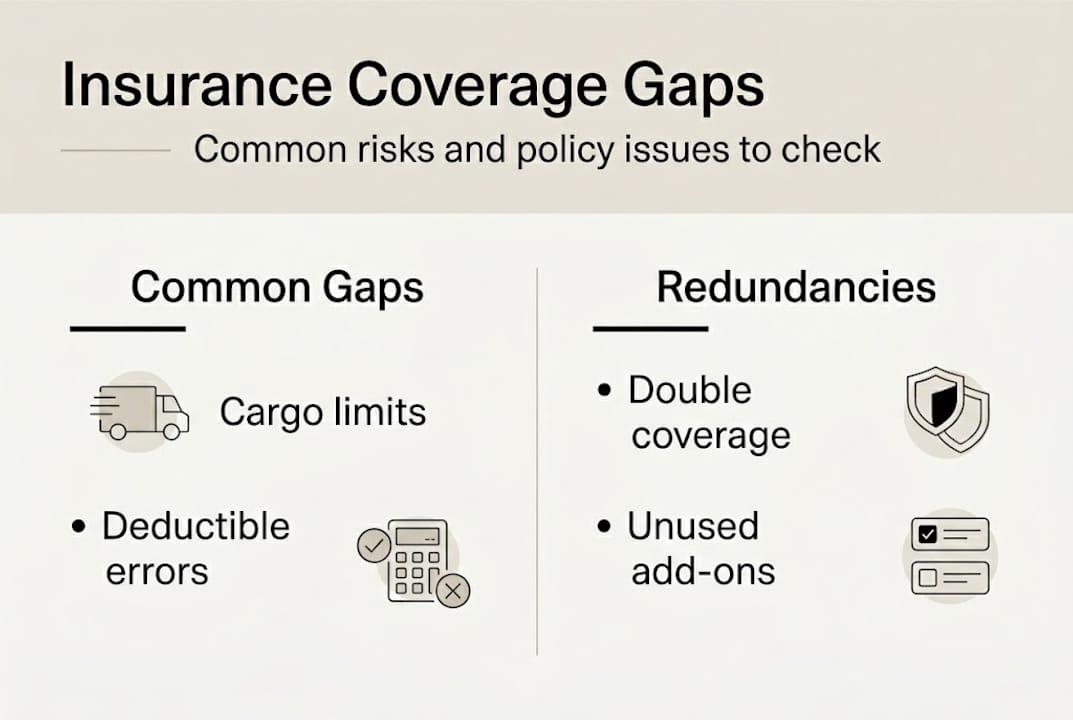

Understanding insurance coverage basics also helps you spot gaps or redundancies in your current policy structure. A redundant endorsement costs money every month.

Risk factor | Potential premium impact |

One at-fault accident | +25% to +50% for 3-5 years |

Poor CSA score (above 65%) | +15% to +30% |

Driver with recent violation | +10% to +20% per driver |

Lapse in coverage | +20% to +40% |

Here is a number that should get your attention: small claims can raise premiums 25-50% for three to five years. That means a $4,000 claim could cost you $15,000 or more in added premiums over the following years. Knowing this changes how you approach every incident.

Pro Tip: Never drop below the minimum coverage levels recommended by your broker just to save a few hundred dollars per month. The short-term savings rarely outweigh the exposure you take on, especially in cargo liability.

For a broader view of protecting your business through smart coverage choices, review your policy annually, not just at renewal.

Shop around and use trucking insurance specialists

With a solid understanding of your current risks and coverage, the next step is to shop smarter, not just cheaper. There is a real difference between a generalist broker who handles auto, home, and commercial lines and a trucking specialist who lives in this market every day.

Here is a step-by-step approach to getting meaningful competitive quotes:

Gather your fleet data including vehicle schedules, driver lists, and loss runs before reaching out to any broker.

Contact at least three brokers, including at least one trucking specialist.

Request itemized quotes so you can compare coverage limits, deductibles, and exclusions side by side, not just total premiums.

Ask each broker about program markets, which are bulk-rate programs designed specifically for trucking fleets.

Negotiate with your preferred carrier using competing quotes as leverage.

Feature | General broker | Trucking specialist |

Access to trucking-specific markets | Limited | Extensive |

Understanding of CSA/ISS impact | Basic | Deep |

Bulk and program rate access | Rare | Common |

Claims advocacy for freight incidents | Generic | Industry-specific |

Compliance guidance included | No | Often yes |

Trucking specialists understand how your comparing insurance quotes process should work differently than a standard commercial fleet. They know which carriers price favorably for owner-operators versus large fleets, and they know which exclusions to watch for in cargo policies.

Pro Tip: Trucking specialists often have access to exclusive program markets that general brokers simply cannot reach. These programs are designed for fleets with specific cargo types, routes, or safety profiles and can offer rates well below standard market pricing.

One warning: the lowest quote is not always the best deal. A policy that excludes refrigerated cargo breakdown or limits your liability on high-value loads can leave you exposed in ways that cost far more than the premium savings.

Improve safety scores and compliance for lower premiums

Comparing providers is key, but your fleet’s safety profile is often the single largest variable affecting what you pay. Insurers use CSA scores as a direct pricing input, and the difference between a good score and a poor one can mean tens of thousands of dollars annually.

CSA scores are the most heavily weighted factor in insurer risk assessment. The three BASICs that matter most for premium pricing are Unsafe Driving, Crash Indicator, and Vehicle Maintenance. Focus your improvement efforts there first.

Steps to improve your scores:

Pull your FMCSA SMS data monthly and identify which violations are driving your scores up.

Challenge inaccurate violations through the DataQs system. Errors are common and correctable.

Implement a pre-trip inspection program with documented checklists for every driver, every day.

Schedule preventive maintenance at manufacturer-recommended intervals and log everything.

Enroll drivers in targeted safety training based on their specific violation history.

CSA score tier | Estimated premium impact |

Below 35% (low risk) | At or below market average |

35-65% (moderate risk) | 10-20% above market average |

Above 65% (high risk) | 25-40% above market average |

FMCSA intervention threshold | Coverage may be restricted |

The results of focused safety investment are real. One fleet’s 22% premium reduction came directly from a structured safety program overhaul, not from switching carriers.

“Insurers do not just look at your score today. They look at the trajectory. A fleet showing consistent improvement over 12 to 18 months is a far better risk in our eyes than one with a static average score.” — Fleet insurance underwriter perspective

Understanding the CSA score impact on your rates is the starting point. Then dig into ISS scores explained to see how roadside inspection selection probability feeds directly into your insurance risk profile. Carriers also monitor ISS scores and costs when evaluating fleet-wide risk.

Leverage technology and data to negotiate better rates

Once your compliance programs are in place, strengthen your negotiating stance by harnessing actionable data. Insurers respond to evidence. A fleet that walks into renewal with documented proof of safety performance is in a fundamentally different negotiating position than one that shows up with nothing but a clean loss run.

Essential data points to track and present:

Telematics reports showing speed, hard braking, and hours-of-service compliance

Driver training completion records with dates and scores

Preventive maintenance logs from your CMMS (Computerized Maintenance Management System)

Incident response documentation showing how quickly and thoroughly you addressed any near-misses

Annual MVR review records for every driver on your policy

Small fleets in particular benefit from this approach. Documented safety programs and CMMS use can help you negotiate 10-20% below actuarial averages, which are the baseline rates insurers use before applying risk adjustments.

“What we want to see from a small fleet is not perfection. It is process. Show us you have systems in place, that you review them, and that you act on what you find. That tells us the risk is managed.” — Commercial trucking underwriter

Pro Tip: Bring your last 12 months of telematics summary reports and your maintenance schedule to every renewal conversation. Most fleets never do this, which means the ones that do stand out immediately and often get better treatment from underwriters.

Choosing the right telematics or CMMS platform matters. Look for systems that export clean, insurer-friendly reports and track the specific metrics your carrier asks about. The premium-reduction strategies that actually move the needle are the ones backed by data you can hand across the table.

Why aggressive insurance cost cutting can backfire: Our take

Every strategy in this guide works. But there is a mindset trap that catches even experienced fleet operators: treating insurance purely as a cost to minimize rather than a risk tool to optimize.

We have seen fleets cut premiums by 18% in year one by dropping endorsements, raising deductibles past their cash reserves, and switching to the cheapest carrier available. Then one serious cargo claim or liability incident wiped out two years of savings in a single check.

The fleets that sustain low insurance costs over time are not the ones who fight hardest for the lowest quote. They are the ones who invest in safety infrastructure, maintain clean records, and build long-term relationships with carriers who understand their operation. Loyalty and documented performance create leverage that no single quote comparison can replicate.

View your insurance spend as part of your risk management budget, not just overhead. The right coverage at a fair price, backed by a carrier who knows trucking, is worth more than the cheapest policy that leaves gaps when you need it most.

Find insurance savings tailored to your fleet’s needs

You now have a clear roadmap: assess your risk profile, shop with specialists, improve your safety scores, and bring data to every renewal conversation. The next logical step is putting these strategies to work with a partner who specializes in exactly this.

At Insuaria, we work exclusively with fleet operators and logistics businesses to build coverage that fits your actual risk exposure, not a generic template. Whether you run five trucks or five hundred, we can help you access custom trucking insurance quotes built around your fleet’s specific profile. Our team knows how to get the best rates without cutting the coverage that protects your business when it matters most. Request your fleet-specific quote today and see what smarter coverage looks like.

Frequently asked questions

What is the most effective way to reduce trucking insurance costs?

Improving safety compliance and working with trucking insurance specialists are the most proven methods, with 10-25% savings achievable when both strategies are combined.

How do safety scores impact trucking insurance premiums?

CSA scores are the most heavily weighted factor insurers use to set rates, and improving your Unsafe Driving, Crash Indicator, and Maintenance BASICs can produce meaningful premium reductions.

Can small claims raise my trucking insurance premiums?

Yes. Small claims can increase premiums 25-50% for three to five years, so every incident decision should factor in the long-term cost of filing versus paying out of pocket.

What documentation helps when negotiating better insurance rates?

Maintenance logs, driver training records, and telematics data are the most persuasive, and documented safety programs can help small fleets negotiate 10-20% below standard actuarial rates.

Recommended

Comments